Quick Answer

“Non VBV” refers to online credit card transactions that bypass the Verified by Visa (VBV) authentication process, which is an added security step designed to protect against fraud. While Non VBV transactions may be faster, they lack this extra layer of verification, potentially increasing the risk of unauthorized use.

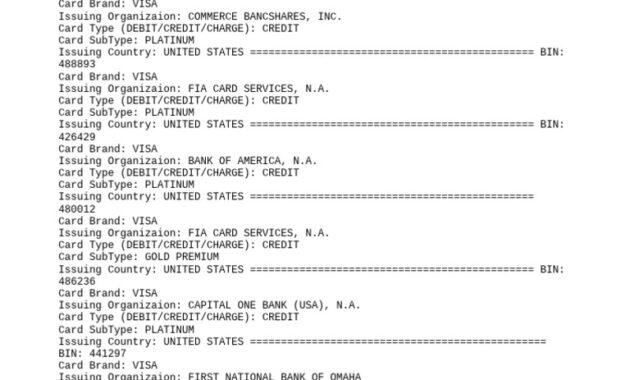

Infobox: Non VBV Transactions at a Glance

| Term | Non VBV (Non Verified by Visa) |

|---|---|

| Definition | Credit card transactions conducted without the Verified by Visa authentication step |

| Purpose of VBV | Enhance security for online purchases via password or code verification |

| Risk Level | Higher potential for fraud compared to VBV transactions |

| Speed | Typically faster due to omission of extra verification |

| Common Usage | Transactions on websites or merchants not enrolled in VBV program |

| Security Alternatives | Other fraud prevention methods may be used by merchants |

Understanding Non VBV Transactions

What is Verified by Visa (VBV)?

Verified by Visa is a security protocol implemented by Visa to add an authentication step during online credit card payments. It typically requires the cardholder to enter a password or a one-time code, confirming their identity and reducing the likelihood of fraudulent transactions.

Defining Non VBV Transactions

Non VBV transactions occur when a credit card purchase is processed without this additional verification step. This means the transaction proceeds without the cardholder having to provide extra authentication, which can streamline the checkout process but may also expose the transaction to greater risk.

Why Non VBV Transactions Matter

In the digital economy, security and convenience often compete. Non VBV transactions highlight this balance by offering faster payment experiences but potentially compromising on fraud protection. Understanding this trade-off is crucial for consumers and merchants alike, as it influences trust, liability, and the overall safety of online commerce.

Common Misconceptions About Non VBV

Myth: Non VBV transactions are always unsafe.

Fact: While they lack VBV’s extra authentication, many merchants employ other security measures to protect customers.

Myth: VBV guarantees 100% fraud protection.

Fact: VBV reduces risk but does not eliminate fraud entirely.

Myth: Non VBV transactions are illegal or unauthorized.

Fact: These transactions are legitimate but simply do not use the VBV protocol.

Practical Example

Consider purchasing a pair of shoes from an online retailer. If the site supports VBV, you might be prompted to enter a password or a code sent to your phone before the payment completes. If the site does not support VBV, the transaction will finalize immediately after entering card details, making the process quicker but with less authentication.

Related Terms

- 3D Secure: A broader security protocol that includes VBV and Mastercard SecureCode.

- Chargeback: A reversal of a credit card transaction initiated by the cardholder or bank.

- Fraud Prevention: Techniques and technologies used to detect and prevent unauthorized transactions.

- Identity Theft: The fraudulent acquisition and use of a person’s private identifying information.

Frequently Asked Questions (FAQ)

Is it safe to make Non VBV transactions?

While Non VBV transactions lack the extra authentication step, many merchants use alternative security measures. However, they generally carry a higher risk of fraud compared to VBV transactions.

Why do some merchants not use Verified by Visa?

Some merchants avoid VBV to simplify the checkout process and reduce cart abandonment, as the extra step can deter some customers.

Can I enable VBV on my card?

VBV is typically activated by the card issuer or bank. Contact your bank to check if your card supports VBV and how to enable it.

What should I do if I suspect fraud on a Non VBV transaction?

Immediately contact your card issuer to report the suspicious activity and request a chargeback if necessary.

Final Answer

Non VBV transactions are online credit card payments processed without the Verified by Visa authentication step, offering faster checkout but with increased exposure to fraud risks. While not inherently unsafe, consumers should weigh convenience against security and consider merchant safeguards before proceeding.

References

- Visa. (n.d.). Verified by Visa. Retrieved from https://usa.visa.com/pay-with-visa/security/verified-by-visa.html

- Federal Trade Commission. (n.d.). Protecting Yourself from Credit Card Fraud. Retrieved from https://consumer.ftc.gov/articles/how-keep-your-credit-card-information-safe

- PCI Security Standards Council. (n.d.). Understanding 3D Secure. Retrieved from https://www.pcisecuritystandards.org/pci_security/3d-secure

Edward Philips offers a thoughtful exploration of the “Non VBV” concept within online transactions, highlighting the critical balance between convenience and security. His analysis underscores the importance of understanding that while Non VBV transactions may streamline the purchasing process by eliminating additional verification steps, they inherently carry increased risks such as fraud and chargebacks. The comparison with VBV, a robust authentication protocol, effectively frames the consumer’s dilemma in today’s digital economy-prioritize speed or safety? Edward also wisely points out that not all Non VBV transactions are inherently unsafe, as many merchants adopt alternative security measures. This nuanced view encourages consumers to remain vigilant, evaluate merchants carefully, and make informed decisions that align with their risk tolerance. Ultimately, this discussion enriches awareness and empowers users to navigate the evolving online marketplace with greater confidence and responsibility.

Edward Philips provides a comprehensive and insightful analysis of the Non VBV phenomenon, shedding light on a crucial issue in contemporary e-commerce: the trade-off between convenience and security. By clearly distinguishing Non VBV transactions from those protected by Verified by Visa protocols, he frames the consumer’s dilemma amid rising cybersecurity concerns. His balanced perspective-that while Non VBV transactions are often faster, they could increase exposure to fraud-encourages shoppers to assess their own risk tolerance carefully. Moreover, highlighting that some merchants implement alternative safeguards offers a refreshing nuance, reminding readers that security isn’t a binary concept. Edward’s exploration empowers consumers to approach online financial activities more mindfully, equipping them to navigate this complex terrain with prudence and confidence in an ever-evolving digital marketplace.

Edward Philips’ examination of Non VBV transactions offers a timely and nuanced insight into the complexities of online payment security. His balanced approach aptly captures the delicate trade-off between the seamless convenience that Non VBV options provide and the heightened security assurances embedded in Verified by Visa protocols. In an era marked by escalating cyber threats, this distinction is pivotal for consumers striving to safeguard their financial information without sacrificing ease of use. Edward’s recognition that Non VBV does not necessarily equate to insecurity-given alternative merchant safeguards-adds critical depth to the conversation. Ultimately, his exploration encourages a proactive mindset where consumers assess risks in alignment with their comfort levels, fostering a more informed and responsible engagement with the digital economy. This perspective is invaluable as both technology and threats evolve, underscoring the ongoing need for vigilance and informed decision-making in online commerce.

Edward Philips’ thoughtful exploration of Non VBV transactions truly illuminates the nuanced interplay between convenience and security in online payments. By distinguishing the Verified by Visa protocol’s robust authentication from Non VBV’s streamlined process, he presents a clear framework for consumers grappling with risk assessment in their digital purchases. His recognition that Non VBV does not inherently mean vulnerability-thanks to alternative safeguards some merchants deploy-introduces an important depth to the discussion often overlooked in mainstream dialogues. This balanced perspective encourages users to evaluate individual risk tolerance and the merchant’s security posture critically, rather than adopting a one-size-fits-all judgment. In an era where cyber threats continually evolve, Edward’s insight fosters a more discerning, responsible approach to digital commerce, prompting consumers to navigate the landscape with both caution and pragmatism.

Edward Philips’ detailed examination of Non VBV transactions provides a vital lens through which consumers can better understand the intricate balance between convenience and security in digital payments. By contrasting the Verified by Visa protocol with Non VBV processes, he sheds light on the risks and benefits inherent to each, emphasizing that while Non VBV may simplify and expedite purchases, it does not guarantee the same level of protection. His acknowledgment that many merchants employ alternative security measures beyond VBV enriches the conversation and avoids oversimplified judgments. This nuanced perspective empowers consumers to make informed choices based on their own risk tolerance and the credibility of merchants. In an era where online fraud is a persistent threat, Edward’s insights serve as a crucial reminder: thoughtful vigilance paired with awareness can help navigate the evolving landscape of online financial security with greater confidence and prudence.

Edward Philips’ articulate analysis of Non VBV transactions sheds essential light on a frequently misunderstood facet of online payments. By delineating the Verified by Visa protocol’s role in fortifying transaction security versus the streamlined yet potentially riskier Non VBV process, he highlights the critical trade-off consumers face between convenience and protection. Importantly, Edward nuances the conversation by acknowledging that Non VBV does not inherently imply insecurity, as many merchants compensate through alternative safeguards. This balanced perspective reinforces the need for consumers to consider their personal risk tolerance and carefully assess merchant credibility when choosing payment methods. His insights prompt a broader reflection on the evolving digital financial landscape, reminding us that vigilance, informed decision-making, and adaptability remain vital in fostering secure and trustworthy e-commerce experiences.

Edward Philips’ article sharpens our understanding of the often-overlooked “Non VBV” transactions within online payments. His insightful unpacking of Verified by Visa’s role as a security layer contrasts effectively with Non VBV’s streamlined-but potentially riskier-approach. This draws attention to the core dilemma many consumers face: opting between a frictionless checkout experience and the fortified protection that VBV provides. Crucially, Edward avoids oversimplification by recognizing that Non VBV does not inherently equate to insecurity, given that many merchants deploy alternative safeguards. This emphasis on nuanced risk assessment urges consumers to move beyond binary thinking and consider not only convenience but also the credibility and security measures of individual merchants. In a digital era rife with cyber threats, his reflections underscore a vital message: informed vigilance, balanced judgment, and adaptive strategies remain essential for fostering trust and safety in e-commerce.

Edward Philips’ comprehensive analysis of Non VBV transactions further enriches the ongoing dialogue about security and convenience in online payments. His detailed distinction between the Verified by Visa authentication protocol and Non VBV transactions demystifies a topic that often confuses consumers. By acknowledging that Non VBV transactions may lack the robust VBV layer yet still employ alternative security measures, Philips encourages a more nuanced and individualized approach to digital payment choices. This insight is especially relevant as cyber threats grow more sophisticated, reminding users that risk assessment extends beyond binary labels of “secure” or “insecure.” Ultimately, Edward’s perspective promotes informed vigilance, urging consumers to weigh their comfort with risk alongside the credibility and security practices of merchants-an essential mindset for navigating today’s complex e-commerce landscape with both confidence and caution.

Edward Philips’ exploration of Non VBV transactions continues to deepen our understanding of the intricate security dynamics in online payments. His analysis adeptly balances the convenience of bypassing Verified by Visa authentication with the inherent risks that this shortcut may carry. Crucially, Edward does not paint Non VBV simply as unsafe; rather, he highlights that many merchants implement other protective measures that can mitigate risks. This perspective is invaluable because it encourages consumers to move beyond a binary view of security and to engage in nuanced risk assessments based on individual comfort levels and merchant credibility. In a digital era marked by escalating cyber threats, Edward’s insights reinforce the importance of informed decision-making and personal vigilance, reminding us that trust in e-commerce requires continual evaluation of both convenience and protection.

Edward Philips’ insightful exploration of Non VBV transactions brilliantly illuminates a critical yet often misunderstood element of online payment security. His balanced approach underscores a key tension: while Verified by Visa (VBV) adds a robust authentication layer enhancing consumer protection, opting for Non VBV transactions can offer quicker, more seamless checkout experiences. Importantly, Philips avoids a simplistic security-vs-convenience dichotomy, noting that many reputable merchants implement alternative protective mechanisms to counterbalance the absence of VBV. This measured perspective encourages consumers to undertake personalized risk assessments, weighing convenience against potential vulnerabilities. In an age of escalating cyber threats and evolving financial technologies, his analysis highlights the indispensable role of informed vigilance. Edward’s work fosters greater consumer empowerment, urging us to approach each transaction as a careful balance between ease and security, a vital mindset for navigating today’s complex digital commerce landscape with confidence and caution.

Edward Philips’ thorough examination of Non VBV transactions significantly enhances our grasp of the delicate balance between convenience and security in online payments. By clearly differentiating Verified by Visa’s explicit authentication from Non VBV’s more streamlined, yet potentially vulnerable, process, he invites consumers to critically evaluate their comfort with risk. What stands out is the recognition that Non VBV does not automatically entail insecurity; many merchants employ alternative protective measures that mitigate potential threats. This nuanced perspective encourages a personalized approach, urging shoppers to assess individual merchants’ security practices rather than adopting a blanket assumption about Non VBV risks. In a digital commerce era marked by advancing cyber threats and evolving payment technologies, Edward’s insights underscore the importance of informed vigilance and thoughtful decision-making to navigate online transactions safely without sacrificing user experience. This balanced view empowers consumers to engage confidently in the digital marketplace.

Edward Philips’ insightful article sheds essential light on the nuanced distinction between VBV and Non VBV transactions, which is often misunderstood in online payments. By emphasizing that Non VBV transactions forego the extra Verified by Visa authentication layer, he highlights a critical security consideration that consumers must consciously weigh against convenience. Importantly, Philips refrains from categorizing Non VBV as inherently unsafe; instead, he thoughtfully points out that many merchants compensate with alternative security measures. This balanced analysis encourages consumers to adopt a discerning mindset-assessing risk relative to personal comfort levels and the credibility of merchants-rather than relying on absolutes. In today’s evolving digital payment landscape, where cyber threats continue to escalate, Edward’s exploration stresses the importance of informed vigilance and flexible decision-making. His work ultimately empowers users to navigate the digital marketplace with both confidence and caution, fostering greater trust and safety in online transactions.

Edward Philips’ article provides a nuanced understanding of Non VBV transactions, highlighting the delicate balance between enhanced security through Verified by Visa and the convenience offered when bypassing it. His thoughtful discussion challenges the simplistic notion that Non VBV equals insecurity by emphasizing that many merchants adopt alternative safeguards. This invites consumers to move beyond binary thinking and engage in personalized risk assessment based on the specific merchant’s practices and their own comfort levels. In an increasingly complex digital payments environment marked by evolving threats, Edward’s insights underscore the importance of informed vigilance and adaptable strategies. Ultimately, this exploration empowers buyers to make smarter choices, reinforcing trust and safety while appreciating the trade-offs between ease of use and robust protection.

Edward Philips’ article adeptly navigates the complex terrain of Non VBV transactions, emphasizing the nuanced trade-off between convenience and security in online payments. By elucidating that “Non VBV” does not inherently imply insecurity but rather represents transactions lacking the Verified by Visa authentication layer, he invites readers to consider a broader spectrum of merchant safeguards beyond this single protocol. This balanced perspective encourages consumers to engage in informed risk assessment tailored to their personal comfort with vulnerability and the specific security measures employed by merchants. In an era where cyber threats continually evolve, Edward’s insights highlight the critical need for adaptive vigilance, reinforcing that while convenience is valuable, it must be weighed thoughtfully against potential exposure. His work ultimately empowers consumers to make deliberate, confident decisions-fostering a safer, more trustworthy digital financial ecosystem.

Edward Philips’ article provides a comprehensive and nuanced analysis of Non VBV transactions, effectively unpacking the complexities that underpin the trade-off between security and convenience in online payments. By clearly distinguishing the Verified by Visa (VBV) authentication layer from Non VBV processes, Edward invites readers to recognize that the absence of VBV does not automatically translate to insecurity. His emphasis on alternative security measures adopted by merchants broadens the conversation beyond a binary understanding, encouraging consumers to apply careful judgment based on their own risk tolerance and the protections in place. In today’s dynamic digital environment, where cyber threats constantly evolve, this thoughtful perspective highlights the importance of informed vigilance-balancing the desire for a swift, hassle-free transaction against the need to safeguard sensitive financial information. Ultimately, Edward’s insights empower consumers to navigate online transactions with greater confidence, fostering safer interactions in the digital marketplace.

Edward Philips’ article astutely unpacks the intricacies of Non VBV transactions, offering a balanced understanding of the security-versus-convenience dilemma in online payments. By clarifying that Non VBV means bypassing the Verified by Visa authentication, he demystifies a term often associated with risk while acknowledging that many merchants deploy alternative safeguards to protect buyers. This nuanced perspective encourages consumers to move beyond simplistic judgments, instead weighing their personal risk tolerance alongside the specific protections a merchant provides. In an environment where cyber threats are constantly evolving, Edward reminds us that convenience should not overshadow security considerations but rather be balanced through informed vigilance. His analysis ultimately equips readers to make smarter, more confident decisions, promoting safer and more trustworthy digital transactions.

Edward Philips’ article articulately illuminates the multifaceted nature of Non VBV transactions, steering the conversation beyond a simplistic security-versus-convenience debate. By clarifying that Non VBV means bypassing the Verified by Visa step rather than outright lacking security, he prompts readers to assess the broader spectrum of protective measures merchants employ. This distinction is vital as it empowers consumers to approach online purchases with a tailored risk assessment rather than default suspicion. Furthermore, Philips thoughtfully highlights the evolving landscape of cybersecurity risks, urging a balanced outlook where convenience does not overshadow vigilance. His analysis enriches our understanding of digital payment mechanisms, encouraging informed decisions that safeguard both consumer interests and trust in the expanding e-commerce ecosystem.

Edward Philips’ article is an insightful exposition on the nuanced landscape surrounding Non VBV transactions, thoughtfully delineating the critical difference between convenience and security in online payments. By clarifying that Non VBV transactions bypass the Verified by Visa step without necessarily lacking security, he encourages consumers to consider the broader array of protective protocols merchants might implement. This approach fosters a more sophisticated risk assessment, moving beyond the simplistic dichotomy of secure versus insecure. In an era rife with evolving cyber threats, Edward’s balanced perspective promotes an informed vigilance-acknowledging that while convenience matters, it must be judiciously weighed against potential vulnerabilities. His analysis ultimately empowers consumers to navigate the increasingly complex digital marketplace with both confidence and prudence, reinforcing the essential interplay between trust, responsibility, and adaptive security measures.

Edward Philips’ article astutely highlights the nuanced dynamics surrounding Non VBV transactions, shedding light on the delicate balance between convenience and security in today’s digital payments landscape. By clarifying that Non VBV means the absence of a specific Verified by Visa authentication step-not necessarily an absence of security-he encourages a more comprehensive evaluation of alternative protective measures merchants may adopt. This distinction empowers consumers to make risk-informed decisions based not solely on a protocol’s presence but on overall security posture and personal comfort with potential vulnerabilities. As cyber threats continue to evolve, Edward’s balanced perspective serves as a timely reminder that opting for speed and simplicity online requires careful consideration and responsibility. Ultimately, his insights foster a deeper awareness and practical vigilance, guiding consumers towards safer and more confident navigation of the complex online financial ecosystem.

Edward Philips offers a thoughtful exploration of the often-misunderstood concept of Non VBV transactions, deftly navigating the delicate balance between convenience and security in online payments. By emphasizing that Non VBV does not inherently mean a lack of protection, he encourages consumers to look beyond the Verified by Visa label and consider a broader range of merchant security measures. This nuanced approach advances the conversation from a simplistic secure-versus-insecure dichotomy to one that values informed risk assessment and personal comfort with online vulnerabilities. His insightful discussion underscores the evolving nature of cybersecurity threats, reminding readers that while speed and simplicity are attractive, they require thoughtful vigilance. Ultimately, Edward’s analysis empowers consumers to engage in the digital marketplace with greater awareness and responsibility, fostering a safer, more resilient financial environment.