Navigating the labyrinthine world of healthcare coverage can feel like traversing a dense jungle, especially when switching between employer-sponsored plans and Affordable Care Act (ACA) marketplaces. The shift isn’t always seamless; it’s a pivotal moment with potential repercussions for your wallet and well-being. Think of your health insurance as a finely tuned engine; changing parts requires understanding the entire mechanism to avoid sputtering and stalls.

Understanding the Interplay: Employer Plans and the ACA

Before diving into the specifics, let’s clarify the distinct roles of employer-sponsored plans and the ACA marketplaces. Employer-provided health insurance, often subsidized, constitutes a significant portion of coverage for working Americans. These plans, negotiated by employers with insurance carriers, offer a range of benefits and cost-sharing arrangements. ACA marketplaces, on the other hand, provide individual and family plans directly to consumers, often with premium tax credits available based on income. Consider the employer plan a steady, reliable current in a river, while the ACA marketplace is a vast, navigable ocean offering more choices, but potentially more turbulent waters.

The Trigger: Life Events and Enrollment Periods

Switching between these two systems typically stems from a life event, a change in circumstances that unlocks special enrollment periods. Job loss, marriage, divorce, birth or adoption of a child, and relocation outside of your existing plan’s service area all qualify as such events. These moments, like unexpected forks in the road, demand careful navigation to ensure continuous coverage. Without a qualifying life event, you generally need to wait for the annual open enrollment period, typically in the fall, to make changes to your health insurance selection.

The Cascade Effect: Potential Impacts of Switching

The act of switching can trigger a cascade of effects on your healthcare costs, coverage levels, and access to care. Let’s examine some key considerations:

1. Continuity of Care: One of the immediate concerns is maintaining continuous access to your healthcare providers. Switching plans may mean that your preferred physician or specialist is no longer in-network, leading to higher out-of-pocket costs or the need to find new healthcare professionals. This is akin to uprooting a plant; it needs time to re-establish its roots in new soil.

2. Deductibles and Out-of-Pocket Maximums: Employer-sponsored plans and ACA marketplace plans operate on different calendar years and may have varying deductible and out-of-pocket maximums. If you switch mid-year, you may need to satisfy a new deductible before your coverage kicks in fully. Similarly, you’ll need to track your out-of-pocket expenses under the new plan to avoid unexpected costs. This is comparable to resetting the odometer in a car; you’re starting fresh with a new set of metrics.

3. Prescription Drug Coverage: Formularies, the lists of covered prescription drugs, vary significantly between plans. A medication covered under your employer plan may not be covered, or may be subject to higher cost-sharing, under an ACA marketplace plan, and vice-versa. It’s crucial to review the formulary of any new plan to ensure access to your essential medications. Think of it as checking the compatibility of a software program with your operating system; not all programs work seamlessly.

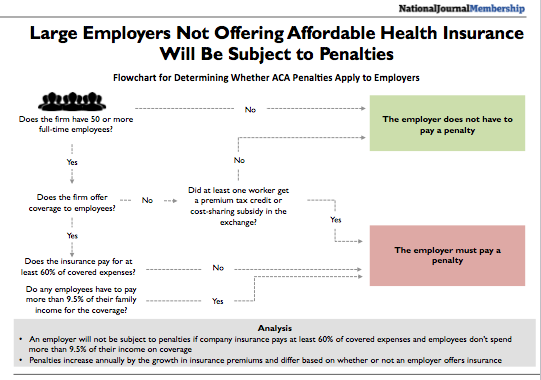

4. Tax Credits and Subsidies: A significant advantage of ACA marketplace plans is the availability of premium tax credits and cost-sharing reductions for eligible individuals and families. These subsidies, based on income and household size, can significantly reduce the cost of coverage. However, eligibility for these subsidies depends on whether you have access to affordable employer-sponsored coverage. If your employer plan is deemed affordable (generally, if the employee’s share of the premium for self-only coverage is less than a certain percentage of household income), you may not be eligible for subsidies on the marketplace. This is akin to having a safety net with variable elasticity; its availability depends on your specific circumstances.

5. Coordination of Benefits: In some situations, you may have both an employer-sponsored plan and an ACA marketplace plan simultaneously. In these cases, it’s essential to understand how the plans coordinate benefits. Typically, one plan is designated as the primary payer, and the other as the secondary payer. The primary payer processes claims first, and the secondary payer may cover some remaining expenses, depending on the policy terms. This intricate dance between two coverage systems requires careful attention to avoid confusion and potential billing errors.

Strategic Considerations for a Seamless Transition

To navigate this intricate landscape successfully, consider these proactive strategies:

1. Plan Ahead: Whenever possible, anticipate potential coverage changes and research your options well in advance. Compare the benefits, costs, and provider networks of different plans to make an informed decision. This is like charting a course before setting sail; preparation is paramount.

2. Understand Enrollment Deadlines: Be aware of special enrollment period deadlines and the effective dates of coverage. Missing a deadline could leave you without coverage for a period, exposing you to significant financial risk. These deadlines are like the ebb and flow of tides; miss them, and you risk being stranded.

3. Document Everything: Keep meticulous records of your enrollment decisions, plan documents, and communications with insurers. This documentation can be invaluable in resolving any disputes or discrepancies that may arise. Think of it as creating a detailed map of your journey; it will help you retrace your steps if needed.

4. Seek Expert Guidance: Don’t hesitate to seek assistance from healthcare navigators, insurance brokers, or benefits specialists. These professionals can provide personalized guidance and help you navigate the complexities of the healthcare system. They are like seasoned guides who know the terrain intimately.

5. Utilize Online Resources: The federal government and many state governments offer online tools and resources to help you compare plans, estimate costs, and determine eligibility for subsidies. These resources can empower you to make informed decisions about your healthcare coverage. They act as a digital compass, pointing you in the right direction.

Switching between employer plans and ACA marketplace plans is a multifaceted process that demands careful attention and planning. By understanding the potential impacts and adopting proactive strategies, you can navigate this transition successfully, ensuring continuous access to affordable, quality healthcare. Remember, your health insurance is not just a policy; it’s a vital component of your overall well-being, demanding thoughtful stewardship.