Imagine your hard-earned savings as seeds meticulously planted in the fertile ground of a financial institution. You nurture them, anticipating a bountiful harvest of financial security. But what happens if a tempestuous storm, an unforeseen economic downturn, threatens to wash away your carefully cultivated field? This is where the Federal Deposit Insurance Corporation (FDIC) steps in, acting as a stalwart guardian, ensuring that your deposited funds remain safe and accessible, even when the financial weather turns turbulent. Understanding the intricate tapestry of FDIC coverage is paramount in navigating the complex landscape of modern finance, offering a bulwark against potential losses and fostering peace of mind.

The Bedrock of Protection: What’s Insured?

The FDIC’s protective embrace extends to a wide array of deposit accounts held at insured banks and savings associations. Think of these as designated plots within your financial garden, each entitled to a certain level of safeguard.

- Checking Accounts: These are the workhorses of your financial life, the accounts you use for everyday transactions. From paying bills to purchasing groceries, funds held in checking accounts are fully insured.

- Savings Accounts: The cornerstone of any prudent financial plan, savings accounts, regardless of their purpose – emergency funds, future down payments – are protected.

- Money Market Deposit Accounts (MMDAs): Offering a blend of liquidity and potentially higher interest rates, MMDAs provide a safe haven for your short-term savings, sheltered under the FDIC umbrella.

- Certificates of Deposit (CDs): These time-bound investments, where you agree to keep your funds locked in for a specified period, earn fixed interest and enjoy the full faith and credit of the FDIC.

- Negotiable Order of Withdrawal (NOW) Accounts: Similar to checking accounts, NOW accounts earn interest and are insured, providing an added incentive for holding funds in a transactional account.

- Official Bank Checks, Cashier’s Checks, and Money Orders: These payment instruments, issued by the bank, represent a guaranteed transfer of funds and are covered until they are cashed or deposited.

Essentially, if it’s a deposit account held at an FDIC-insured institution, it’s highly likely to be shielded from loss, up to the established coverage limit.

The Shielding Threshold: Understanding Coverage Limits

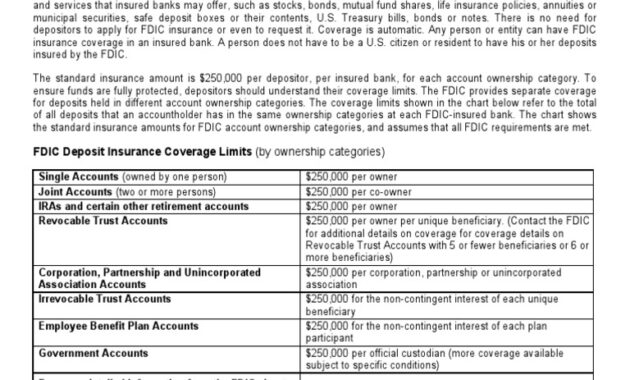

The standard deposit insurance coverage limit is currently $250,000 per depositor, per insured bank. This isn’t merely a number; it’s a critical demarcation line, a safeguard against catastrophic loss. It’s akin to having a sturdy levee protecting your farmland from flooding – as long as the water level stays below the levee’s height, your crops remain safe.

However, the FDIC’s coverage paradigm allows for potential expansion beyond this baseline. By understanding the nuances of ownership categories, you can strategically structure your accounts to maximize your protection.

Navigating Ownership Categories: Expanding Your Protective Canopy

The FDIC recognizes various ownership categories, each with its own set of rules and coverage allowances. Mastering these intricacies is like learning the art of origami, allowing you to fold and manipulate your accounts to achieve maximum protection.

- Single Accounts: These are accounts owned by one person, and they are insured up to $250,000.

- Joint Accounts: Accounts owned by two or more individuals are insured up to $250,000 per owner. This means a joint account with two owners can be insured for up to $500,000, and so on. This assumes all owners have equal rights to withdraw funds.

- Revocable Trust Accounts: These accounts, often used for estate planning, offer unique opportunities for amplified coverage. The amount insured depends on the number of beneficiaries and their relationship to the grantor (the person establishing the trust). This is where the waters get a bit murkier, requiring careful consideration of the trust’s structure.

- Irrevocable Trust Accounts: Similar to revocable trusts, but with the key distinction that the trust cannot be altered or terminated by the grantor after its creation. Coverage depends on the beneficiaries and their vested interests in the trust.

- Retirement Accounts: Certain retirement accounts, such as Individual Retirement Accounts (IRAs) and self-directed 401(k)s, held at insured institutions, are also insured up to $250,000 per owner. Note that this coverage applies to the deposit accounts held within these retirement plans, not the underlying investments (stocks, bonds, etc.).

Understanding these ownership categories and how they interact with FDIC coverage is paramount. It’s not merely about passively accepting the standard $250,000 limit; it’s about actively sculpting your financial landscape to achieve optimal protection.

Beyond the Horizon: What’s Not Covered?

While the FDIC’s shield is broad and robust, it doesn’t encompass every financial instrument under the sun. Certain asset types fall outside its protective range, representing areas where caution and due diligence are crucial.

- Stocks, Bonds, and Mutual Funds: These investments, inherently subject to market fluctuations, are not insured by the FDIC. Their value can rise or fall, and the FDIC offers no guarantee against losses.

- Life Insurance Policies: The cash value of life insurance policies is not FDIC-insured.

- Annuities: These contracts, designed to provide a stream of income in retirement, are not covered by the FDIC.

- Cryptocurrencies: The burgeoning world of cryptocurrencies exists outside the FDIC’s purview. Digital currencies like Bitcoin and Ethereum are not insured, making them susceptible to significant risk.

Recognizing these exclusions is just as important as understanding what is covered. It’s about creating a well-diversified portfolio that balances risk and reward, with FDIC-insured deposits forming a solid foundation.

The Takeaway: A Prudent Approach to Financial Security

The FDIC insurance is a cornerstone of financial stability, offering a tangible safeguard against unforeseen economic shocks. It’s the bedrock upon which you can build a secure financial future. By understanding the scope of coverage, the nuances of ownership categories, and the limitations of the insurance, you can make informed decisions that protect your hard-earned savings and cultivate a flourishing financial landscape.