Quick Answer

The Residual Dividend Model (RDM) is a financial strategy where companies distribute dividends only from leftover earnings after funding all profitable investment opportunities, prioritizing growth over immediate shareholder payouts.

Infobox: Residual Dividend Model at a Glance

| Aspect | Details |

|---|---|

| Definition | Dividend payments made from residual earnings after capital investments |

| Primary Focus | Reinvestment of earnings for growth |

| Dividend Variability | Fluctuates based on investment opportunities |

| Investor Appeal | Long-term growth-oriented shareholders |

| Cost of Equity Role | Determines reinvestment feasibility |

| Common Outcome | Lower or irregular dividends but potential for capital appreciation |

Overview of the Residual Dividend Model

The Residual Dividend Model represents a strategic framework in corporate finance that treats dividend payments as secondary to funding profitable projects. Instead of distributing a fixed portion of earnings, companies following this model allocate capital first to internal growth opportunities. Dividends are then paid out only from the remaining, or residual, earnings. This approach underscores the importance of reinvestment in enhancing a company’s long-term value rather than focusing solely on immediate shareholder returns.

Why the Residual Dividend Model Matters

This model is significant because it aligns dividend policy with a company’s growth strategy and financial health. By prioritizing reinvestment, firms can fund projects that generate returns exceeding their cost of capital, fostering sustainable expansion. For investors, understanding this model helps in evaluating whether a company is focused on long-term value creation or short-term income. It also explains why dividend payments may be inconsistent, reflecting the company’s fluctuating investment needs rather than financial instability.

Common Misunderstandings About the Residual Dividend Model

One frequent misconception is that irregular or low dividends indicate poor company performance. In reality, under the RDM, dividend variability often signals active reinvestment in profitable ventures. Another myth is that all investors prefer steady dividends; however, the model attracts shareholders who prioritize capital gains and long-term growth over immediate income. Additionally, some believe that the model disregards shareholder interests, but it actually balances reinvestment with eventual returns, aiming to maximize shareholder wealth over time.

How the Residual Dividend Model Works

Prioritizing Investment Opportunities

Companies first identify and finance all projects with expected returns above their cost of equity. This ensures that retained earnings are used efficiently to generate value.

Calculating Residual Earnings

After funding these investments, any leftover earnings constitute the residual amount available for dividend distribution.

Dividend Payment Decisions

Dividends are paid only from this residual pool, which can lead to fluctuating dividend amounts depending on the company’s investment pipeline.

Example of the Residual Dividend Model in Practice

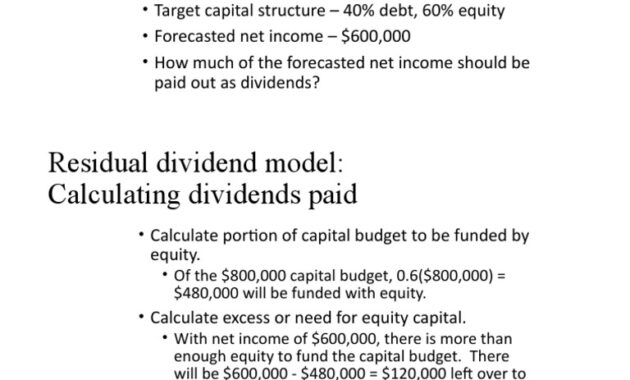

Consider a technology firm that earns $10 million annually. It identifies $7 million worth of projects with returns exceeding its cost of capital. The company allocates this $7 million to reinvestment, leaving $3 million as residual earnings. According to the RDM, the firm would distribute dividends only from this $3 million, resulting in a smaller or variable dividend payout compared to a fixed dividend policy.

Related Terms

- Cost of Equity: The return rate a company must offer investors to compensate for risk.

- Retained Earnings: Profits kept within the company for reinvestment rather than paid out as dividends.

- Dividend Policy: The strategy a company uses to decide how much profit to return to shareholders.

- Capital Budgeting: The process of evaluating and selecting long-term investment projects.

- Capital Appreciation: Increase in the value of an asset or investment over time.

Frequently Asked Questions (FAQ)

Does the Residual Dividend Model mean dividends are always low?

Not necessarily. Dividends may be lower or irregular when investment opportunities are abundant, but can increase when fewer projects require funding.

Is the Residual Dividend Model suitable for all companies?

This model is best suited for firms with significant growth opportunities and fluctuating capital needs, rather than mature companies with stable earnings.

How does the cost of equity affect dividend payments?

A higher cost of equity means fewer projects meet the return threshold, potentially increasing dividends, while a lower cost encourages more reinvestment and smaller dividends.

Can investors rely on dividends for steady income under this model?

Investors seeking consistent income may find the RDM less appealing due to dividend variability; it favors those focused on long-term capital gains.

Final Answer

The Residual Dividend Model prioritizes reinvesting earnings into profitable projects before distributing dividends, resulting in variable payouts aligned with growth opportunities. This approach benefits investors focused on long-term value rather than immediate income, reflecting a company’s strategic commitment to sustainable expansion.

References

- Brealey, R. A., Myers, S. C., & Allen, F. (2020). Principles of Corporate Finance. McGraw-Hill Education.

- Ross, S. A., Westerfield, R. W., & Jaffe, J. (2019). Corporate Finance. McGraw-Hill Education.

- Damodaran, A. (2012). Investment Valuation: Tools and Techniques for Determining the Value of Any Asset. Wiley.

- Investopedia. (n.d.). Residual Dividend Model. Retrieved from https://www.investopedia.com/terms/r/residualdividendmodel.asp

Edward Philips offers a compelling exploration of the Residual Dividend Model (RDM), emphasizing its strategic significance in corporate finance. By framing dividends as the “residual” earnings after necessary investments, he highlights how this approach prioritizes sustainable growth over immediate shareholder payouts. This perspective challenges traditional views of dividends as guaranteed returns, inviting investors to appreciate the nuanced balance between reinvestment and distribution. Philips’ analogy of investors as gardeners discerning whether a company is nurturing its roots or trimming leaves vividly clarifies the model’s essence. Furthermore, his insight into the inherent dividend volatility under RDM underscores the importance of aligning investor expectations with corporate strategies. Ultimately, this analysis deepens our understanding of how dividend policies reflect a firm’s commitment to long-term value creation rather than short-term gratification.

Building on Curtis Cole’s insightful reflections, Edward Philips’ analysis of the Residual Dividend Model brilliantly captures the delicate balance companies strike between growth and shareholder rewards. By emphasizing that dividends arise only after funding profitable projects, Philips invites investors to see dividends not as entitlements but as indicators of a firm’s reinvestment priorities and strategic vision. His metaphor of investors as gardeners skillfully conveys the importance of patience and discernment, highlighting that sustainable growth often requires foregoing immediate gratification. Additionally, the discussion around dividend volatility sheds light on why some investors may feel unsettled, while others find opportunity in this dynamic framework. Overall, Philips’ exposition enriches our understanding of dividend policy as a dynamic instrument that mirrors a company’s long-term financial health and strategic foresight.

Edward Philips’ comprehensive examination of the Residual Dividend Model (RDM) profoundly enriches the discourse on corporate dividend policies by revealing the strategic underpinnings that inform dividend decisions. His portrayal of dividends as residual outcomes, contingent upon the funding of lucrative investment opportunities, elegantly underscores the primacy of growth and value maximization. The analogy of investors as attentive gardeners is particularly evocative, inviting a thoughtful reconsideration of shareholder patience and the trade-offs between immediate income and future capital appreciation. Furthermore, Philips insightfully addresses the often misunderstood volatility in dividend payments, demonstrating how this reflects a company’s adaptive response to fluctuating investment prospects rather than instability. By linking dividend policy to a firm’s cost of equity and reinvestment discipline, this analysis offers investors a robust framework to evaluate corporate health and strategic foresight. Overall, Philips’ work compellingly encourages a long-term, growth-oriented investor perspective within the complex dynamics of dividend strategy.

Edward Philips’ insightful analysis of the Residual Dividend Model (RDM) lucidly captures the nuanced balance companies maintain between reinvestment and shareholder returns. By portraying dividends as the “leftover” earnings after funding profitable projects, Philips reframes dividend payments as strategic choices rather than obligations. This perspective encourages investors to adopt a long-term mindset, appreciating how retained earnings fuel sustainable growth and enhance intrinsic company value. The analogy of investors as gardeners is particularly powerful, illustrating the need for patience and prudent judgment in evaluating dividend policies. Moreover, Philips’ explanation of dividend volatility demystifies fluctuations, revealing them as adaptive responses to changing investment opportunities rather than instability. His linkage of dividend decisions to the firm’s cost of equity further enriches our understanding of capital allocation and strategic foresight. Overall, this thoughtful exposition deepens investor appreciation of how RDM aligns dividend policy with enduring corporate health and value maximization.

Edward Philips’ detailed exploration of the Residual Dividend Model (RDM) offers a profound lens through which dividend policies can be understood-not as fixed entitlements but as deliberate residual outcomes shaped by strategic reinvestment priorities. By emphasizing that dividends emerge only after all value-accretive investments are funded, Philips underscores the model’s alignment with sustainable corporate growth and prudent capital allocation. His evocative gardener analogy powerfully illustrates the investor’s role in discerning between nurturing long-term potential versus seeking fleeting income. Furthermore, Philips adeptly addresses the dividend volatility inherent in RDM, reframing it as a rational response to evolving investment opportunities rather than fiscal inconsistency. This nuanced discussion enriches investor insight into how dividend decisions reflect a firm’s cost of equity, financial health, and commitment to future value creation. Overall, this comprehensive analysis compellingly advocates for a growth-oriented, patient investor mindset grounded in strategic corporate finance principles.

Edward Philips’ elucidation of the Residual Dividend Model (RDM) masterfully deepens our comprehension of dividend policies as strategic mechanisms rather than fixed entitlements. His depiction of dividends as “residual” earnings underscores the primacy of funding growth opportunities first, positioning reinvestment as the cornerstone of sustainable corporate value. The gardener analogy vividly illustrates the patience required by investors to appreciate long-term nurturing over immediate rewards, highlighting a critical mindset shift. Moreover, Philips’ explanation of dividend volatility as a rational reflection of shifting investment prospects clarifies why dividend payments may fluctuate without signaling instability. By linking dividend decisions to a firm’s cost of equity and strategic foresight, this analysis offers investors a robust framework to evaluate corporate health and capital allocation. Overall, Philips compellingly advocates embracing the RDM to foster a growth-focused and discerning investment approach grounded in corporate financial realities.

Edward Philips’ thorough exploration of the Residual Dividend Model (RDM) adds a vital dimension to how we interpret dividend policies-not as static promises but as strategic decisions reflecting a company’s reinvestment priorities and growth potential. His analogy of dividends as “residual” earnings after funding valuable projects reinforces the idea that sustainable growth takes precedence over immediate payouts. By likening investors to gardeners, Philips vividly captures the patience and foresight required to assess whether a firm is cultivating long-term strength or simply providing short-term yield. Additionally, his insight into the inherent volatility of dividends under RDM challenges conventional expectations of predictability, framing such fluctuations as rational responses to shifting investment landscapes. Linking dividend policy to the firm’s cost of equity further deepens our understanding of capital allocation, making this analysis an essential guide for investors aiming to align their strategies with a company’s financial health and future prospects.

Edward Philips’ insightful exposition on the Residual Dividend Model (RDM) significantly advances our understanding of dividend policy as a strategic, growth-focused decision rather than a mere distribution mechanism. By framing dividends as earnings leftover after funding all value-adding investments, Philips highlights the primacy of reinvestment in driving sustainable company growth. His gardener analogy artfully depicts the investor’s role in exercising patience and discernment, reinforcing the importance of evaluating a firm’s long-term vitality over short-term payouts. Additionally, Philips’ exploration of dividend volatility clarifies why fluctuations are natural within RDM, reflecting a company’s adaptive capital allocation rather than instability. The linkage of dividend decisions to the firm’s cost of equity further enriches this analysis by situating dividend policy within the broader context of financial strategy and market conditions. Overall, this comprehensive and nuanced discussion equips investors to align expectations with corporate priorities, fostering a more informed and forward-looking investment approach.

Edward Philips’ comprehensive treatise on the Residual Dividend Model (RDM) profoundly reframes dividends as strategic reflections of a company’s reinvestment priorities rather than mere shareholder handouts. By illustrating that dividends arise only after funding all value-creating projects, Philips spotlights the essential trade-off between immediate payouts and sustainable growth. His gardener metaphor eloquently conveys the investor’s role in recognizing whether a firm nurtures its foundational assets or focuses on short-term returns. The discussion on dividend volatility further enriches this view, explaining fluctuations as rational outcomes of shifting investment prospects rather than financial instability. Importantly, Philips integrates the firm’s cost of equity into the analysis, providing a critical measure to gauge reinvestment attractiveness and dividend policy rationale. This nuanced exploration equips investors with a robust conceptual framework to balance patience with prudent assessment, emphasizing long-term value creation over fleeting income gratification.

Building on Edward Philips’ thorough exposition, the Residual Dividend Model (RDM) fundamentally reframes dividend policy as a strategic culmination rather than a fixed obligation. This model’s insistence that dividends flow only from earnings left after funding profitable investments foregrounds a company’s commitment to sustainable growth, rather than short-term shareholder appeasement. Philips’ compelling gardener metaphor captures the nuanced investor mindset required-balancing patience with discernment to appreciate how reinvestment nourishes long-term value creation. Furthermore, the acknowledgment of dividend volatility as a rational reflection of changing investment prospects demystifies fluctuations that often unsettle income-focused investors. By integrating the company’s cost of equity as a vital benchmark, Philips equips investors with a clear metric to evaluate reinvestment attractiveness and dividend strategies. Ultimately, this perspective urges a recalibration of investor expectations-favoring long-term capital appreciation over immediate payouts and deepening engagement with corporate financial strategy.

Building on Edward Philips’ compelling exposition, the Residual Dividend Model (RDM) serves as an insightful framework that elevates dividend policy beyond simple cash returns to shareholders. By positioning dividends as the residual outcome after all profitable investments are funded, the model underscores a company’s strategic focus on sustainable growth rather than immediate shareholder gratification. Philips’ gardener metaphor poignantly captures the investor’s role in exercising patience and discernment, recognizing whether a company is nurturing its core assets through reinvestment or merely offering short-term payouts. Furthermore, the RDM’s acknowledgment of dividend volatility as a principled response to shifting investment opportunities demystifies common investor concerns. Importantly, the integration of the cost of equity as a benchmark deepens our understanding of how firms balance reinvestment and dividends. Ultimately, Philips’ analysis encourages investors to adopt a long-term horizon, aligning their expectations with a company’s growth potential and strategic capital allocation.

Edward Philips’ articulation of the Residual Dividend Model offers a profound lens through which to view dividend policies-not as fixed payouts but as dynamic outcomes shaped by corporate investment priorities. His framing that dividends should only emerge from earnings leftover after funding viable projects reinforces the model’s core emphasis on sustainable growth over short-term returns. The metaphor of investors as gardeners is particularly striking, vividly illustrating the patience and strategic insight required to discern whether a company is cultivating its foundational assets or prioritizing immediate dividends. Furthermore, Philips’ discussion on dividend volatility elucidates common investor anxieties by contextualizing fluctuations as a rational reflection of evolving investment opportunities rather than instability. Integrating the cost of equity into this analysis adds depth, positioning dividend decisions within a broader framework of financial efficiency and strategic foresight. Altogether, this exposition enriches our appreciation of dividend policy as a sophisticated signal of corporate vitality and long-term value creation.

Edward Philips’ detailed exploration of the Residual Dividend Model (RDM) deepens our comprehension of dividend policy as a strategic exercise rooted in corporate growth priorities. By emphasizing that dividends are a residual outcome-issued only after all value-generating investments have been funded-he reframes dividend payments as indicators of financial health and reinvestment discipline rather than mere cash rewards. The gardener metaphor vividly captures the patience and insight investors need to gauge whether a company is cultivating long-term value or seeking immediate gratification. Philips’ insights on dividend volatility clarify that fluctuations stem from shifting investment opportunities, not necessarily instability, offering reassurance to informed investors. Moreover, linking dividend policy to the cost of equity adds a vital dimension, contextualizing the allocation between reinvestment and payouts within broader financial efficiency metrics. Overall, this analysis invites investors to adopt a long-term perspective, aligning with sustainable corporate growth and strategic capital allocation.

Edward Philips’ insightful analysis elegantly underscores the Residual Dividend Model’s role as a strategic framework that transcends traditional dividend paradigms. By positioning dividends as the leftover earnings after all value-adding investments, he highlights a company’s deliberate prioritization of growth and reinvestment, which in turn signals financial vigor rather than mere cash distribution. His metaphor of investors as gardeners cultivating underlying strength aptly captures the patience and acuity needed to evaluate whether a firm is nurturing sustained value or merely offering superficial rewards. Philips also thoughtfully addresses the inherent volatility in dividend payments, reframing it not as instability but as a consequence of tactical capital allocation responsive to evolving opportunities. Moreover, his integration of the cost of equity as a decision-making benchmark enriches this perspective, linking dividend policy directly to corporate financial strategy. This comprehensive exposition invites investors to embrace a long-term, growth-oriented mindset that aligns with sound corporate stewardship.

Edward Philips’ insightful analysis of the Residual Dividend Model (RDM) masterfully articulates the intricate balance between corporate growth and shareholder returns. By framing dividends as the surplus after all viable investments have been financed, Philips emphasizes that dividend policy is not a mere distribution decision but a strategic reflection of a firm’s reinvestment priorities and financial health. His vivid gardener metaphor underscores the patience and discernment investors must exercise to understand whether a company is genuinely cultivating sustainable value or simply offering transient gratification. Furthermore, by addressing dividend volatility as a natural consequence of shifting investment opportunities rather than instability, Philips reframes investor expectations around payout fluctuations. Importantly, situating the cost of equity at the heart of this model enriches the analytical framework, allowing investors to evaluate dividend decisions in light of financial efficiency and strategic foresight. This holistic exposition encourages a long-term, growth-focused perspective that aligns with sound capital stewardship.