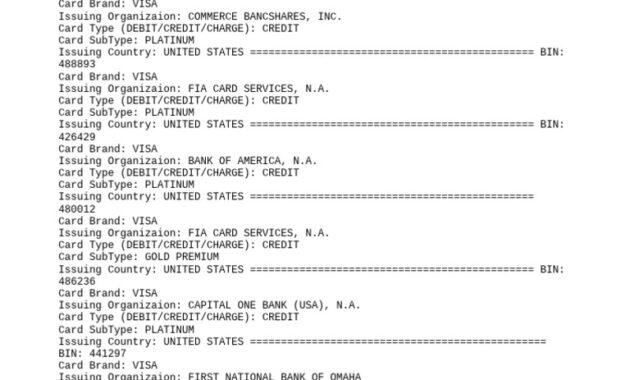

In the realm of online transactions and financial activities, the term “Non VBV” surfaces frequently, engendering an array of inquiries. But what does it signify specifically? The acronym “VBV” stands for “Verified by Visa,” an authentication protocol designed to bolster security for online purchases. Conversely, a “Non VBV” transaction refers to credit card transactions that do not utilize this additional layer of verification. This absence can raise questions about the safety and reliability of such transactions.

Imagine, if you will, attempting to purchase an item online and navigating the labyrinth of security measures. You are presented with a screen enforcing VBV authentication, a protective mechanism that instills a sense of safety. But there, glimmering amidst the complexity, is the “Non VBV” option. Does this signify a smoother transaction process, or does it herald potential jeopardy?

Non VBV transactions, while often quicker and ostensibly more straightforward, omit the robust validation present in VBV systems. This raises potential challenges, particularly for consumers wary of online fraud. Credit card companies and merchants that do not employ VBV may find themselves exposed to a higher risk of chargebacks, fraudulent purchases, or identity theft. In an age where cybersecurity is a paramount concern, the absence of VBV could be perceived as a double-edged sword.

While many consumers may seek convenience and speed, they must also consider the implications of engaging in a Non VBV transaction. Navigating these waters requires a judicious approach. Not all Non VBV transactions are fraught with danger; in fact, many reputable merchants implement alternative security measures. Carefully examining a merchant’s security precautions may unveil a tapestry of protective mechanisms, albeit not under the umbrella of VBV.

As one delves deeper into the intricacies of Non VBV transactions, it becomes evident that one must weigh the pros and cons meticulously. The convenience of not having to input an additional security code juxtaposes the potential exposure to online threats. Consumers may ponder their comfort level with risk. Are the savings in time and effort worth the possible peril?

Ultimately, understanding the distinction between VBV and Non VBV not only aids in informed purchasing decisions but also cultivates a broader awareness of the online financial landscape. Each transaction becomes an expedition through a realm filled with both convenience and caution, evoking the timeless adage: with great power comes great responsibility. As the digital marketplace continues to evolve, so too must the strategies employed by both consumers and merchants to foster an environment characterized by trust and security.