Quick Answer

The elimination period in long-term care insurance is a designated waiting timeframe after eligibility during which the insured must cover care expenses out-of-pocket before benefits begin. Its length varies by policy and impacts premium costs and financial planning.

Infobox: Elimination Period in Long-Term Care Insurance

| Term | Elimination Period (Waiting Period) |

|---|---|

| Definition | Timeframe after benefit eligibility during which insured pays care costs independently |

| Typical Duration | 30 days to several months |

| Purpose | Risk management for insurers; ensures benefits are used by those with genuine care needs |

| Effect on Premiums | Shorter periods increase premiums; longer periods reduce premiums |

| Factors Influencing Length | Age, health status, anticipated care requirements |

Overview of the Elimination Period

The elimination period, often called the waiting period, is a crucial feature of long-term care insurance policies. It represents the span of time that must pass after a policyholder qualifies for benefits before the insurer begins to cover care costs. During this interval, the insured is responsible for paying all expenses related to their care. The length of this period can differ widely, typically ranging from one month to several months, depending on the terms of the insurance contract.

Why the Elimination Period Is Important

This waiting period serves as a protective mechanism for insurance providers, helping to reduce the risk of unnecessary or premature claims. By requiring policyholders to cover initial care costs, insurers ensure that benefits are reserved for those with genuine, ongoing long-term care needs. For consumers, understanding this period is vital because it directly affects both the cost of premiums and the financial readiness required to manage care expenses during the waiting time.

Balancing Costs and Coverage: Choosing the Right Elimination Period

Deciding on the length of the elimination period involves weighing immediate financial capacity against future uncertainties. Opting for a shorter waiting period means benefits start sooner but usually results in higher monthly premiums. Conversely, a longer elimination period lowers premium payments but demands that the insured have sufficient savings or resources to cover care costs during the waiting phase. This decision should be made with careful consideration of personal finances and anticipated health needs.

Factors Influencing the Elimination Period

Several elements can affect the choice and length of the elimination period. Age is a significant factor, as older individuals are more likely to require long-term care sooner. Health status and the expected type and duration of care also play roles in determining an appropriate waiting period. Tailoring the elimination period to these personal circumstances helps ensure that the insurance plan aligns with both care needs and financial stability.

Common Misunderstandings About the Elimination Period

- Myth: The elimination period is the same for all policies.

Fact: It varies widely depending on the insurer and specific policy terms. - Myth: No benefits are paid during the elimination period.

Fact: Correct, but some policies may offer partial coverage or alternative benefits during this time. - Myth: A shorter elimination period is always better.

Fact: While it provides quicker access to benefits, it often comes with higher premiums, which may not suit everyone’s budget.

Practical Example

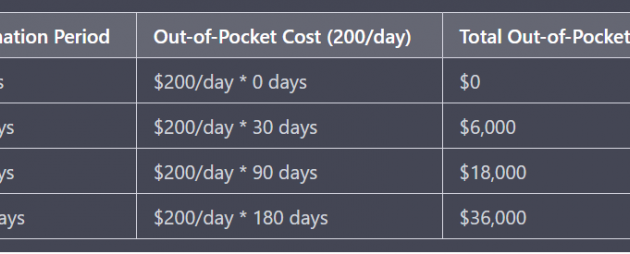

Consider Jane, a 65-year-old planning for future care needs. She chooses a 90-day elimination period to keep her premiums affordable. This means if Jane requires long-term care, she must pay for the first three months herself before her insurance benefits begin. Jane ensures she has savings set aside to cover this period, balancing cost savings with preparedness.

Related Terms

- Long-Term Care Insurance: Insurance designed to cover services related to chronic illness or disability.

- Premium: The amount paid periodically to maintain an insurance policy.

- Benefit Eligibility: The conditions under which an insured person qualifies to receive insurance benefits.

- Waiting Period: Another term for elimination period, often used interchangeably.

Frequently Asked Questions (FAQ)

- Can the elimination period be waived?

- In some cases, policies offer a waiver of the elimination period under specific conditions, such as hospitalization, but this varies by insurer.

- Does the elimination period apply to all types of care?

- Typically, it applies to long-term care services, but the exact coverage depends on the policy details.

- How does the elimination period affect premium costs?

- Shorter elimination periods generally increase premiums, while longer periods reduce them.

- Is the elimination period the same as a deductible?

- No, the elimination period is a time-based waiting period, whereas a deductible is a fixed amount paid before benefits apply.

Final Answer

The elimination period is a waiting timeframe in long-term care insurance during which the insured must pay for care out-of-pocket before benefits commence. Its length influences premium costs and requires careful financial planning. Selecting the right elimination period balances immediate affordability with future care needs.

References

- National Association of Insurance Commissioners (NAIC). “Long-Term Care Insurance Model Act.”

- AARP. “Understanding Long-Term Care Insurance.”

- Insurance Information Institute. “Long-Term Care Insurance Basics.”

- U.S. Department of Health & Human Services. “Long-Term Care Services.”