Navigating the choppy waters of bounced checks can be a significant challenge for any accounting department. A rejected payment disrupts the financial equilibrium, demanding swift and judicious action. But what if I told you that bounced checks, often viewed as mere nuisances, could actually become opportunities for improved internal controls and enhanced customer relationships? Let’s explore how to transform these financial hiccups into stepping stones for a more robust and efficient accounting process. Are you ready to delve into the nuances of handling these returned instruments?

I. Understanding the Genesis of the Bounce: Root Cause Analysis

Before diving headfirst into rectifying the situation, a thorough investigation into the reason for the check’s dishonor is paramount. Was it a case of insufficient funds (NSF), a closed account, a stop payment order, or perhaps a more mundane issue such as a mismatched signature or a technical glitch at the bank? This diagnostic phase is critical. Identifying the underlying cause dictates the subsequent course of action. Insufficient funds are the most frequent culprit, but dismissing other possibilities outright would be a grave error. A meticulous examination of the returned check’s details and a prompt communication with the payer can often unveil the truth. Consider this akin to a forensic accounting investigation on a miniature scale.

II. The Initial Response: Prompt Notification and Account Freezing

Upon receiving notification of a bounced check from your financial institution, time is of the essence. The first step is to immediately notify the customer or payer about the dishonored payment. This communication should be clear, concise, and professional, outlining the reason for the rejection and the amount due, including any applicable fees. Concurrently, it is prudent to temporarily freeze the customer’s account to prevent further transactions until the outstanding balance is settled. This safeguard prevents compounding the issue and protects the organization from additional financial exposure. Failure to act swiftly can result in a snowball effect, complicating the recovery process.

III. Recouping the Funds: Strategies for Recovery

Several avenues exist for recovering the funds from a bounced check. The most straightforward approach is to request the payer to issue a new payment, preferably via a more secure method such as a wire transfer, certified check, or electronic funds transfer (EFT). Another option is to redeposit the original check, but only after confirming with the payer that sufficient funds are now available. This avoids incurring additional fees and further damaging the relationship. For larger sums or recurring issues, a formal payment plan might be necessary, outlining a schedule of installments for repayment. In extreme cases, where all other attempts fail, pursuing legal action might be the only recourse, but this should be considered a last resort due to the associated costs and potential impact on the customer relationship.

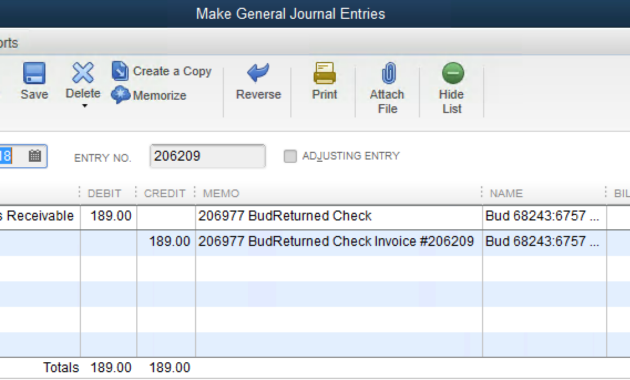

IV. Accounting Adjustments: Reversing the Transaction and Recording Fees

The accounting department must meticulously reverse the initial entry that credited the customer’s account for the amount of the bounced check. This involves debiting the accounts receivable account and crediting the cash account. Simultaneously, any fees incurred due to the bounced check, such as bank charges, should be recorded as an expense. A separate general ledger account might be created specifically for “bounced check fees” to track these costs effectively. Proper documentation is crucial. Maintain a detailed record of all communications, actions taken, and associated expenses related to each bounced check. This information is invaluable for auditing purposes and for identifying patterns that might indicate systemic issues.

V. Implementing Preventative Measures: Mitigating Future Occurrences

Prevention is always better than cure. Implementing robust preventative measures can significantly reduce the incidence of bounced checks. Encourage customers to utilize electronic payment methods whenever possible, as these are less susceptible to errors and fraud. Implement a check verification system that screens checks for common red flags, such as outdated account information or suspicious signatures. Establish clear payment policies and procedures that outline the consequences of bounced checks, including fees and potential account suspension. Regularly review and update these policies to reflect best practices and emerging trends in payment processing. Furthermore, consider implementing a grace period for first-time offenders, offering them an opportunity to rectify the situation without incurring immediate penalties. This can foster goodwill and maintain a positive customer relationship.

VI. Leveraging Technology: Automation and Integration

Modern accounting software offers a plethora of tools for automating the process of handling bounced checks. Integration with banking systems allows for real-time notification of rejected payments, triggering automated workflows for notification and recovery. Some software packages also include features for tracking communication with customers, managing payment plans, and generating reports on bounced check activity. Embracing these technological advancements can streamline the process, reduce manual errors, and improve overall efficiency.

VII. Refining Internal Controls: Strengthening the Foundation

Bounced checks can often be indicative of weaknesses in internal controls. Use each incident as an opportunity to review and strengthen these controls. Are proper procedures in place for verifying customer information? Are employees adequately trained in detecting fraudulent checks? Is there sufficient segregation of duties to prevent errors or manipulation? A thorough review of internal controls can identify vulnerabilities and lead to the implementation of more effective safeguards. This proactive approach not only reduces the risk of bounced checks but also enhances the overall integrity of the accounting process.

VIII. Cultivating Customer Relationships: Turning Setbacks into Opportunities

While bounced checks are undeniably frustrating, they also present an opportunity to strengthen customer relationships. Handle each situation with professionalism, empathy, and a focus on finding a mutually agreeable solution. Avoid accusatory language and instead focus on understanding the customer’s perspective. Offer flexible payment options and be willing to work with customers to resolve the issue. By demonstrating a commitment to fairness and understanding, you can transform a potentially negative experience into a positive one, fostering loyalty and goodwill. Remember, customer perception is paramount.

In conclusion, handling bounced checks in accounting requires a multifaceted approach that encompasses investigation, notification, recovery, accounting adjustments, preventative measures, technology utilization, internal control refinement, and customer relationship management. By viewing these incidents not as mere annoyances but as opportunities for improvement, organizations can transform these financial hiccups into stepping stones for a more robust, efficient, and customer-centric accounting process. Embrace the challenge, and watch your financial landscape transform. The key is to remain agile and adaptable, continuously refining your strategies to meet the ever-evolving demands of the financial world. What seemingly begins as a headache, with proper planning, is a key area for growth.

This comprehensive guide brilliantly transforms the often frustrating issue of bounced checks into a strategic advantage for organizations. By emphasizing a root cause analysis, it encourages accounting teams to understand why payments fail, which is crucial for tailored solutions. The emphasis on prompt communication and account freezing highlights the importance of swift, proactive measures to minimize financial risk. I appreciate the detailed recovery strategies that balance firmness with flexibility, aiming to preserve customer relationships, which is often overlooked. The focus on accounting accuracy and tracking fees ensures transparency and ease in audits. Furthermore, advocating for prevention through policy, verification, and embracing technology showcases how modern tools can revolutionize traditional processes. Strengthening internal controls and fostering empathy with customers rounds out a holistic approach, turning setbacks into sustainable growth opportunities. This piece encourages a mindset shift from problem-solving to opportunity-seeking-a valuable perspective for any finance professional.

This insightful article masterfully reframes bounced checks from a disruptive problem into a valuable catalyst for improvement. By advocating thorough root cause analysis, it encourages accounting teams to move beyond surface-level fixes and tailor responses that address the real issues. The prompt notification and precautionary account freeze demonstrate prudent risk management, balancing firm control with customer respect. I particularly appreciate the emphasis on combining recovery efforts with customer empathy-offering flexible payment options fosters goodwill rather than alienation. The integration of technology and automation not only streamlines workflows but also enhances accuracy and accountability, essential in today’s fast-paced financial environment. Moreover, reinforcing internal controls based on lessons learned ensures long-term resilience. Ultimately, this comprehensive approach turns a common challenge into an opportunity for operational excellence and stronger client relationships, exemplifying strategic thinking in financial management.

Joaquimma-anna’s article offers a well-rounded exploration of handling bounced checks, elevating what is typically seen as a mere nuisance to a strategic focal point for operational enhancement. The methodical breakdown-from understanding root causes to leveraging technology and refining internal controls-provides a clear, actionable roadmap for finance teams. I find the emphasis on blending rigorous financial procedures with empathetic customer engagement particularly compelling, as it underscores the importance of preserving relationships while safeguarding organizational interests. Additionally, the stress on documentation and the thoughtful use of automation reflects a modern, efficient approach that addresses both accuracy and scalability. This piece not only equips accounting departments with practical tools but also advocates a proactive, opportunity-driven mindset that can transform recurring challenges into meaningful improvements in workflow, risk mitigation, and client trust.

Joaquimma-anna’s article offers an impressively thorough and strategic approach to managing bounced checks, which are frequently dismissed as mere transactional setbacks. What stands out is the holistic framework that spans from meticulous root cause analysis to leveraging cutting-edge automation, all while maintaining a customer-centric focus. The emphasis on prompt, professional communication combined with practical recovery options strikes the right balance between protecting financial interests and nurturing client relationships. I especially value the call to use bounced checks as a lens to strengthen internal controls and refine processes, which elevates accounting from a reactive function to a proactive driver of organizational resilience. Additionally, advocating for preventative measures and continuous policy updates reflects a forward-thinking mindset essential in today’s evolving financial landscape. This article not only equips professionals with actionable insights but also reframes challenges as catalysts for growth and improved collaboration.