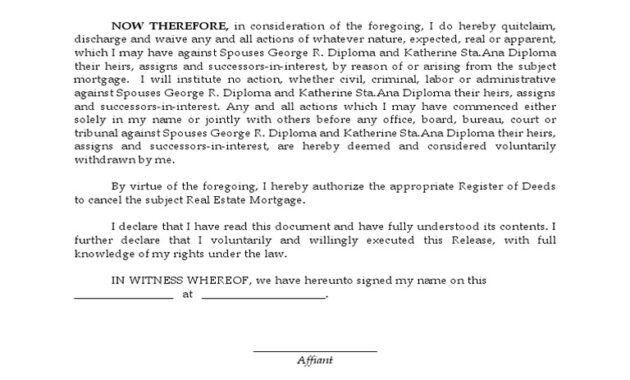

Quick Answer

The release of mortgage, also known as mortgage discharge, is the official process confirming that a borrower has fully repaid their home loan. It legally removes the lender’s claim on the property, restoring full ownership rights to the homeowner and marking the end of mortgage obligations.

Infobox: Release of Mortgage at a Glance

| Term | Release of Mortgage (Mortgage Discharge) |

|---|---|

| Definition | Legal confirmation that a mortgage loan has been fully repaid and the lender’s lien on the property is removed. |

| Also Known As | Mortgage discharge, mortgage satisfaction |

| When It Occurs | After the borrower completes all payments including principal, interest, and fees. |

| Key Parties | Borrower (homeowner), lender (mortgagee), local land records office |

| Legal Effect | Clears the title of the property from mortgage encumbrance |

| Impact on Credit | Positive reflection on credit history |

Overview

The release of mortgage is a formal legal procedure that signifies the end of a mortgage contract between a borrower and a lender. Once the borrower has paid off the entire loan amount, including any interest and fees, the lender issues a release document. This document is then recorded with the relevant government authority, such as a land registry or county recorder’s office, to officially remove the lender’s lien on the property. This process confirms that the homeowner now holds clear and unencumbered title to their property.

Legal and Financial Significance

Legal Confirmation of Ownership

By recording the release of mortgage, the lender formally relinquishes all claims to the property. This legal step is essential to prevent any future disputes or misunderstandings regarding ownership. Without this recorded release, third parties might still consider the mortgage active, potentially complicating property sales or refinancing.

Financial Implications

Successfully completing the mortgage and obtaining a release can positively influence a borrower’s credit profile, demonstrating responsible financial behavior. It also opens opportunities for future borrowing or refinancing, as the property is no longer encumbered by debt. This financial freedom can be a foundation for new investments or economic activities.

Emotional and Social Impact

Beyond the legal and financial aspects, the release of mortgage carries deep emotional significance. Homeownership is often associated with stability, achievement, and personal success. Paying off a mortgage is a milestone that symbolizes years of dedication, budgeting, and perseverance. For many, it marks a transformative moment where the dream of fully owning a home becomes a reality, fostering a sense of pride and security.

Common Misunderstandings

- Myth: The mortgage is automatically released once the final payment is made.

Fact: The lender must prepare and file the release document with the appropriate authority to legally clear the mortgage. - Myth: The release of mortgage affects the property’s market value.

Fact: While it clears ownership, the market value depends on other factors like location and condition. - Myth: The release process is immediate.

Fact: It can take several weeks for the release to be recorded and reflected in public records.

Example

Consider Jane, who purchased her home with a 30-year mortgage. After years of consistent payments, she makes her final payment. The lender then issues a release of mortgage document, which is recorded with the county recorder’s office. Jane now holds a clear title to her home, free from any lender claims, allowing her to sell or refinance without restrictions.

Related Terms

- Mortgage Lien: A legal claim by a lender on a property until the loan is repaid.

- Title Clearance: The process of ensuring a property’s title is free from liens or encumbrances.

- Mortgage Satisfaction: Another term for the release of mortgage.

- Refinancing: Replacing an existing mortgage with a new loan, often with better terms.

Frequently Asked Questions (FAQ)

How long does it take to get a release of mortgage after the final payment?

The timeframe varies by lender and jurisdiction but typically ranges from a few days to several weeks for the release to be prepared and officially recorded.

Is there a fee for recording the release of mortgage?

Some local governments charge a nominal fee to record the release document, though this cost is usually minimal.

Can a homeowner sell their property before the mortgage is released?

Yes, but the mortgage must be paid off at closing, and the release recorded to transfer clear title to the buyer.

What happens if the release of mortgage is not recorded?

If not recorded, the mortgage lien may still appear on public records, potentially complicating future transactions or refinancing.

Why It Matters

Understanding the release of mortgage is vital for homeowners and buyers alike, as it ensures clear property ownership and protects against legal disputes. It also marks a significant financial achievement, enabling greater economic flexibility and peace of mind.

Final Answer

The release of mortgage is the official legal process that confirms a mortgage loan has been fully repaid and removes the lender’s claim on the property. This milestone not only clears the homeowner’s title but also symbolizes financial freedom and personal accomplishment, paving the way for future opportunities.