Quick Answer

A non-embedded deductible in health insurance means the entire family shares one combined deductible amount before coverage begins, rather than each member having an individual deductible. This can lead to higher out-of-pocket costs but may simplify budgeting for some families.

Infobox: Non-Embedded Deductible Overview

| Feature | Description |

|---|---|

| Definition | Single deductible amount shared by the whole family |

| Applies To | Family health insurance plans |

| Deductible Payment | Paid collectively by all family members |

| Out-of-Pocket Maximum | Often higher compared to embedded deductibles |

| Impact on Coverage | Insurance starts paying only after full family deductible is met |

| Common in | Family plans without individual deductibles |

Understanding Deductibles in Health Insurance

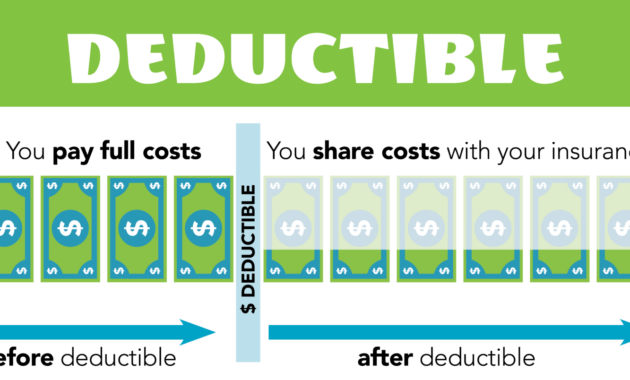

A deductible is the sum an insured person must pay out-of-pocket for medical services before their insurance provider begins to cover expenses. Deductibles can be structured in different ways, especially in family plans, where they may be either embedded or non-embedded.

What Is a Non-Embedded Deductible?

In a non-embedded deductible arrangement, the entire family shares one combined deductible amount. This means the family as a whole must meet the total deductible before the insurance company starts paying for any member’s healthcare costs. Unlike embedded deductibles, where each individual has a separate deductible limit, non-embedded deductibles require collective spending to reach the threshold.

Why Non-Embedded Deductibles Matter

This deductible type significantly influences how families manage healthcare expenses. Since the deductible applies to the family unit collectively, a single member’s high medical costs contribute toward the family’s total deductible. However, until the full family deductible is met, no insurance benefits apply to any member, which can delay coverage and increase out-of-pocket spending.

Financial Implications for Families

Families with non-embedded deductibles may face challenges such as:

- Higher upfront costs: The entire family must meet the deductible before coverage begins.

- Increased out-of-pocket maximums: These plans often have higher limits, potentially leading to substantial expenses.

- Budgeting complexity: Managing healthcare costs requires careful planning and communication among family members.

Common Misunderstandings

- Myth: Each family member has their own deductible in a non-embedded plan.

Fact: The deductible is shared collectively by the entire family.

- Myth: Insurance pays for one member’s care once their individual expenses reach a certain amount.

Fact: Insurance only starts paying after the total family deductible is met.

- Myth: Non-embedded deductibles always cost more.

Fact: While they can lead to higher out-of-pocket costs, some families prefer the simplicity of a single deductible.

Example Scenario

Consider a family of four with a $5,000 non-embedded deductible. If one member incurs $3,000 in medical bills and the others have minimal expenses, the family still needs to pay an additional $2,000 collectively before insurance coverage begins for any member. This contrasts with embedded deductibles, where the individual with $3,000 in expenses might have met their personal deductible and started receiving benefits.

Related Terms

- Embedded Deductible: Individual deductibles within a family plan that count toward a family maximum.

- Out-of-Pocket Maximum: The maximum amount a family or individual pays before insurance covers 100% of costs.

- Coinsurance: The percentage of costs the insured pays after meeting the deductible.

- Premium: The monthly payment to maintain health insurance coverage.

Frequently Asked Questions (FAQ)

Q: Can a family member receive insurance benefits before the family deductible is met in a non-embedded plan?

A: No, benefits begin only after the entire family deductible is satisfied.

Q: Are non-embedded deductibles more common in family or individual plans?

A: They are typically found in family health insurance plans.

Q: How can families manage costs with a non-embedded deductible?

A: By budgeting carefully, using preventive care, and coordinating medical visits to optimize expenses.

Final Answer

A non-embedded deductible requires the entire family to meet a single deductible amount before insurance coverage starts, which can lead to higher upfront costs but may simplify financial planning for some families. Understanding this structure is essential for making informed decisions about family health insurance options.

References

- Healthcare.gov. (n.d.). Understanding Deductibles. Retrieved from https://www.healthcare.gov/glossary/deductible/

- Kaiser Family Foundation. (2023). Health Insurance Deductibles and Out-of-Pocket Costs.

- Investopedia. (2024). Embedded vs. Non-Embedded Deductibles in Health Insurance.