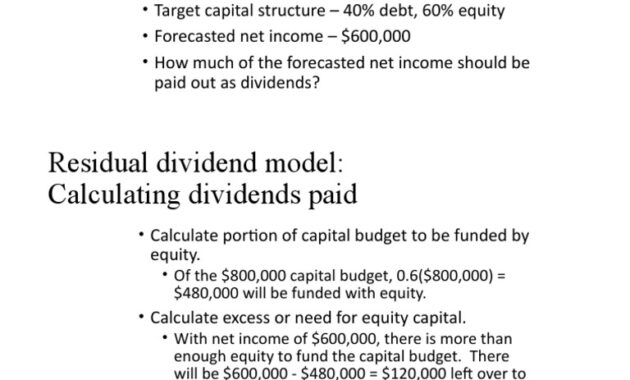

The Residual Dividend Model (RDM) emerges as a unique financial paradigm, akin to a navigational compass in the tumultuous seas of corporate finance. It serves as a guiding principle for investors, highlighting that dividends are not mere monetary distributions but rather reflections of a company’s fiscal health. This model delineates a clear distinction between retained earnings and dividend payouts, shedding light on the intricate interplay of corporate reinvestment and shareholder returns.

At its core, the Residual Dividend Model posits that dividends should only be issued from earnings that remain after all viable investment opportunities have been funded. This “residual” nature of dividends suggests a prioritization of internal investment over external distributions, aligning with the quintessential adage of “putting the cart before the horse.” By adopting this paradigm, companies may illustrate a robust commitment to growth, thereby enhancing their long-term value. Investors, resembling astute gardeners, must discern whether the company is nurturing its roots through reinvestments or merely trimming its leaves for immediate satisfaction.

The implications of this model are profound for investors. It operates on the premise that a company should retain earnings to plow back into projects that yield a higher return than the cost of capital. For the discerning investor, this delineates a dual-edged sword; while immediate payouts may be less frequent, the prospect of future growth could yield more substantial dividends in the long run. Thus, the RDM appeals to those with an appetite for long-term appreciation over short-term gratification.

Moreover, the model propounds a clear rationale for the volatility often witnessed in dividend payments. Unlike fixed-income securities, where payouts are predictable, companies adhering to the RDM may alter their dividends based on available investment opportunities. This dynamic can evoke anxiety among investors attuned to regular income flows, yet it also cultivates a selective population of investors who appreciate the underlying corporate strategy and its potential for capital appreciation.

Intriguingly, the RDM also highlights the significance of the company’s cost of equity. As a yardstick for potential reinvestment opportunities, a lower cost of equity may encourage companies to retain more earnings for growth initiatives. Consequently, this model becomes a lens through which investors can assess not only a firm’s financial health but also its strategic foresight. By analyzing a company’s dividend policy through the prism of the Residual Dividend Model, investors gain insights into the firm’s prioritization of growth versus immediate returns.

In conclusion, the Residual Dividend Model stands as a testament to the philosophy that the true value of a company lies not just in its current returns, but in its capacity for sustainable growth. This nuanced approach compels investors to recalibrate their expectations and embrace a longer-term perspective, ultimately enriching their engagement in the ever-evolving landscape of corporate finance.