In the realm of accounting, the term “outstanding” emerges as a potent descriptor, signifying that which is not yet settled or completed. This multifaceted adjective takes on a myriad of interpretations, reflecting the dynamic nature of financial transactions and obligations. Much like a painter’s canvas waiting to be filled with vibrant hues, outstanding items on a balance sheet denote an essential stage in the life cycle of financial dealings.

At its core, the concept of outstanding represents those assets or liabilities that linger in a state of incompletion. For example, when a business issues an invoice, the amount due becomes an outstanding receivable until payment is collected. Similarly, bills and obligations exist as outstanding liabilities until they are duly settled. This duality of outstanding items creates a narrative that intertwines revenue and expenditure, revealing the intricate ballet of cash flows within an organization.

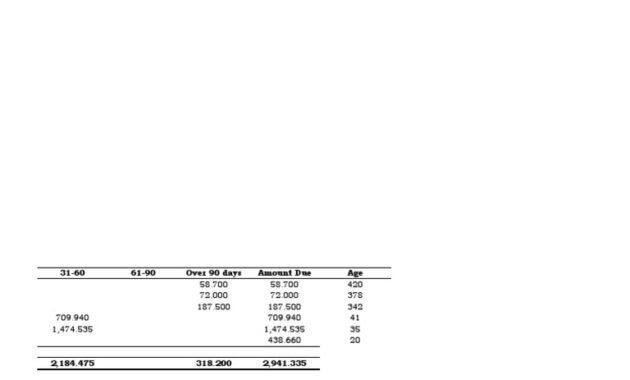

Examining accounts receivable, the outstanding balance serves as a beacon of anticipated revenue. It symbolizes trust—the promise that debts will be honored, and cash will eventually grace the ledger. However, an excessive amount of outstanding receivables could cast a shadow on an organization’s liquidity, reminiscent of a fog obscuring a once-clear path. Investors and stakeholders closely scrutinize these figures, as a protracted period for collections not only impacts cash flow but also signals potential inefficiencies or broader market dynamics that may require attention.

On the flip side, outstanding payables represent obligations awaiting fulfillment, akin to unfinished symphonies that echo within a company’s fiscal landscape. This liability signifies a commitment to suppliers and creditors, illustrating the need for strategic cash management. A prudent approach to managing outstanding payables can result in favorable relationships with vendors, while mismanagement may precipitate a downward spiral of reputational risk and compromised financial stability.

The duality present in outstanding metrics complicates the narratives of success or failure in financial stewardship. This is where the art of accounting showcases its unique appeal—transforming mere numbers into stories of opportunity and caution. Whether viewed through the lens of anticipated income or required payments, outstanding items necessitate a careful balance of foresight and prudence.

In conclusion, the term outstanding in accounting encapsulates the essence of anticipation and obligation. This nuanced term serves as a constant reminder of the importance of efficient financial management. By artfully navigating the landscape of outstanding items, organizations craft an insightful portrait of their economic health, one that resonates with the rhythms of commerce and the inexorable flow of time.