Imagine your business as a meticulously crafted ship, sailing smoothly on the ocean of commerce. Each transaction is a ripple, propelling you forward. But a bounced check? That’s a rogue wave, threatening to disrupt your course. Fear not! Navigating this choppy water is easier than you think, especially with QuickBooks as your trusty compass.

Entering a bounced check into QuickBooks isn’t just about accounting; it’s about maintaining the integrity of your financial records and protecting your business from unnecessary losses. A bounced check, often referred to as a non-sufficient funds (NSF) check, represents a payment that a bank refuses to honor due to insufficient funds in the payer’s account. Ignoring it or mishandling the entry can lead to discrepancies, inaccurate reporting, and a distorted view of your financial health. It’s like trying to build a castle on quicksand; the foundation simply won’t hold.

Here’s a step-by-step guide to properly record a bounced check in QuickBooks, ensuring your financial ship stays afloat:

I. Identifying the Leviathan: Recognizing the Bounced Check

Before you can remedy the situation, you need to identify the bounced check. The bank will typically notify you, often providing a physical return of the check or an electronic notification. Be diligent in reviewing your bank statements and transaction logs. The notification will often include details such as the check number, the date of the check, and the reason for the rejection. This information is crucial for accurate record-keeping.

II. Charting the Course: Creating a “Bounced Check” Item

To streamline the process, create a specific item in QuickBooks dedicated to handling bounced checks. Think of it as your designated lifeboat for these financial mishaps. Here’s how:

- Navigate to the “Lists” menu and select “Item List.”

- Click the “Item” button at the bottom and choose “New.”

- Select “Service” as the item type.

- Name the item something descriptive, such as “Bounced Check Fee” or “NSF Charge.”

- In the “Account” field, select an appropriate expense account, such as “Bank Charges” or “Miscellaneous Expenses.” This is where the bounced check fee will be categorized.

- Optionally, enter a description for the item, such as “Fee charged for returned check.”

- Click “OK” to save the item.

This item will be used to record the fee that the bank charges you for the bounced check, which is distinct from the original amount of the check.

III. Reversing the Tide: Reversing the Original Invoice Payment

The initial step is to undo the entry that recorded the customer’s payment. It’s like rewinding time to the moment before the storm hit. This is vital to ensure your accounts receivable accurately reflect the outstanding balance. Follow these steps:

- Find the original invoice that the customer paid with the bounced check.

- Open the invoice and locate the payment that was applied to it.

- Click on the payment to open it.

- In the payment window, click the “Delete” button (or “Void,” depending on your QuickBooks version) to remove the payment from the invoice. This will effectively reinstate the invoice as unpaid.

- Click “Save” to confirm the change.

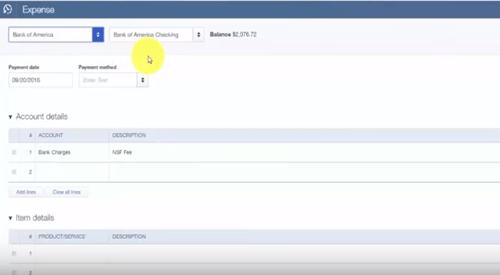

IV. Levying the Toll: Recording the Bank Fee

Now, record the fee that your bank charged you for the bounced check. This is a separate expense that needs to be accounted for. Utilize the “Bounced Check Fee” item you created earlier.

- Go to the “Banking” menu and select “Enter Bills.”

- Enter the bank’s name as the vendor.

- Enter the date of the bank fee.

- In the “Expenses” tab, select the “Bounced Check Fee” item from the dropdown menu.

- Enter the amount of the bank fee in the “Amount” column.

- Add a memo describing the fee, such as “Bank fee for returned check # [Check Number].”

- Click “Save & Close.”

This ensures that the bank fee is properly recorded as an expense and categorized appropriately.

V. Informing the Mariner: Notifying the Customer

Inform your customer about the bounced check and the associated fees. This is crucial for maintaining a healthy business relationship. Be professional and clear in your communication.

VI. Recalibrating the Compass: Creating a New Invoice or Charge

Issue a new invoice or charge to the customer that includes the original amount of the bounced check plus any fees you are charging them. This is like setting a new course for the ship.

- Create a new invoice for the customer.

- Add a line item for the original amount of the invoice that was paid with the bounced check.

- Add another line item for any bounced check fees you are charging the customer. Use the “Bounced Check Fee” item if you want to pass along the bank fee.

- Provide a clear explanation in the invoice memo, such as “Re-issuance of invoice # [Original Invoice Number] due to returned check.”

- Save and send the invoice to the customer.

VII. Watching the Horizon: Monitoring the Outstanding Balance

Keep a close eye on your accounts receivable to ensure the customer pays the new invoice promptly. Follow up with reminders if necessary. This is like keeping a vigilant watch on the horizon for any potential storms.

VIII. Sailing Smoothly: Preventing Future Bounced Checks

While occasionally inevitable, steps can be taken to minimize the occurrence of bounced checks. Consider offering alternative payment methods, such as electronic transfers or credit card payments, which often have lower rates of return. Implement a clear payment policy that outlines the consequences of bounced checks. Regular communication with your customers about their payment status can also help prevent misunderstandings and delays.

Handling bounced checks in QuickBooks doesn’t have to be a daunting task. By following these steps, you can efficiently manage these financial hiccups, maintain accurate records, and keep your business sailing smoothly towards success. Remember, a well-maintained financial ship is a resilient one, capable of weathering any storm.