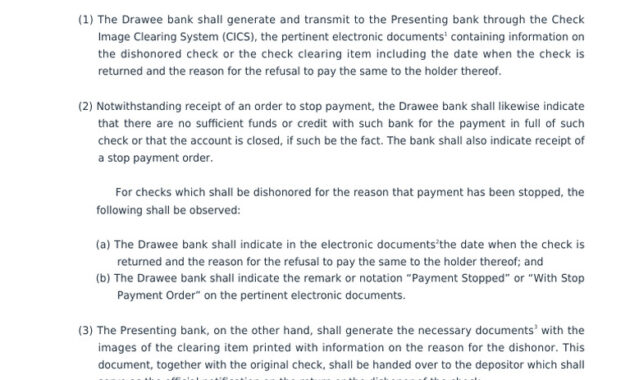

Ever feel that sinking sensation, a gut-wrenching premonition, when you realize a check you wrote might be bouncing back like a rogue boomerang? The insidious specter of returned check fees looms large for many, a financial pitfall that can quickly drain your coffers. But fear not, intrepid financial navigator! This guide is your lodestar, charting a course through the treacherous waters of insufficient funds and equipping you with the armaments to ward off those pesky fees.

I. Master Your Account Balance: The Keystone of Avoidance

The single most crucial element in evading returned check fees is a scrupulous understanding of your account balance. This isn’t just a cursory glance at your online banking app; it’s a deep dive into your financial ecosystem. Let’s dissect this further:

A. Real-Time Monitoring: Your Financial Clairvoyance. Embrace the digital age and utilize online banking tools to monitor your account activity in real-time. Set up alerts for low balances; many banks offer this service, providing an early warning system before you dip into the red. This is a preventative measure, a financial Heimdall watching the Bifrost of your bank account.

B. Reconcile Your Statements with Scrupulous Precision. Don’t just blindly trust the bank statement. Each month (or more frequently, if you’re prone to writing checks), meticulously compare your records against the bank’s. Uncover discrepancies, identify outstanding checks that haven’t cleared, and flag any unauthorized transactions. This forensic accounting will give you a clearer picture of your true available balance.

C. Understand Provisional Credits and Holds. Banks often place temporary holds on deposited funds, or extend provisional credit before funds are fully available. Be acutely aware of these holds and the timeframe before the funds become accessible. Writing a check against funds that are technically in your account but not yet available is a recipe for a returned check fee disaster. Prudence is paramount here.

II. Embrace the Digital Revolution: Alternatives to the Antiquated Check

The humble paper check, a relic of a bygone era, is increasingly being superseded by more efficient and secure digital alternatives. Consider adopting these modern modalities to minimize the risk of returned checks:

A. Direct Debit and Electronic Funds Transfers (EFTs). For recurring payments like utilities, rent, or loan installments, opt for direct debit. These automated transfers eliminate the possibility of a bounced check due to forgetfulness or timing issues. It’s like putting your finances on autopilot.

B. Bill Pay Services: Your Digital Scribe. Most banks offer online bill pay services. You can schedule payments in advance, ensuring they are processed on time and with sufficient funds. This is especially useful for irregular bills where the amount fluctuates.

C. Digital Payment Platforms: Venmo, PayPal, and Zelle. For payments to individuals, embrace the convenience of digital payment platforms. These platforms offer instantaneous transfers, eliminating the need for checks altogether. They are the digital handshake of the 21st century.

III. Strategize Your Spending: Proactive Financial Management

Sometimes, even with the best intentions, unexpected expenses arise. Strategic planning can help you navigate these situations without resorting to writing checks you can’t cover:

A. Overdraft Protection: A Safety Net, Not a Hammock. Sign up for overdraft protection, linking your checking account to a savings account or line of credit. This provides a buffer if you inadvertently overdraw your account. However, be aware that overdraft protection may come with fees of its own, so use it judiciously. It’s a lifeline, not a free pass.

B. Negotiate Payment Due Dates. If you’re facing a temporary cash flow crunch, contact your creditors and inquire about adjusting payment due dates to better align with your payday. Many companies are willing to work with you, avoiding the hassle of a returned check. A little communication can go a long way.

C. Prioritize Your Payments: Triage Your Finances. When funds are limited, prioritize essential payments like rent, utilities, and loan installments. These are the cornerstones of your financial stability. Delaying or skipping discretionary expenses can help you avoid bouncing a check on a crucial bill.

IV. Communication is Key: Engage with Your Bank and Payees

Don’t be afraid to engage in open communication with your bank and payees. Transparency can often avert a potential financial mishap:

A. Inform Your Bank of Potential Delays. If you anticipate a delay in a deposit clearing, notify your bank immediately. They may be able to temporarily waive overdraft fees or provide alternative solutions.

B. Contact Payees Before Writing Checks. If you’re unsure whether sufficient funds will be available by the time a check is cashed, contact the payee and explain the situation. They might be willing to hold the check for a few days or accept an alternative payment method.

C. Promptly Address Returned Check Notices. If you do receive a returned check notice, respond promptly and take immediate action to rectify the situation. Paying the amount due and any associated fees as quickly as possible can minimize the long-term damage to your credit rating.

By diligently implementing these strategies, you can significantly reduce the likelihood of incurring returned check fees. Proactive financial management, coupled with a savvy embrace of digital tools, will empower you to navigate the financial landscape with confidence and avoid the dreaded boomerang of a bounced check. So, arm yourself with this knowledge, and may your bank account always be flush with funds!