The allure of financial tables, particularly amortization schedules, often escapes immediate comprehension. Why the fascination with rows and columns delineating the gradual diminution of debt? On the surface, it’s a chronicle of repayment, but delve deeper, and you’ll discover a tapestry woven with threads of financial prudence, predictive modeling, and the reassuring cadence of fiscal responsibility. An amortization schedule is more than just a ledger; it’s a roadmap to debt freedom, a projection of future expenses, and a vital tool for both borrowers and lenders alike.

At its core, an amortization schedule is a table meticulously detailing each periodic payment of a loan. It disaggregates each payment into its constituent parts: the portion allocated to principal reduction and the portion dedicated to interest. This provides a transparent view of how the loan balance diminishes over time, offering a clear picture of the debt’s lifecycle. Essentially, it reveals the quantum of each payment earmarked for interest versus principal, thereby illuminating the true cost of borrowing.

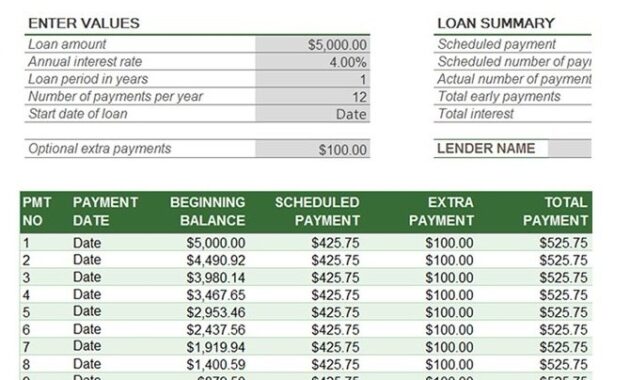

The Anatomy of an Amortization Schedule: Deconstructing the Table

Comprehending the structure of an amortization schedule is crucial to unlocking its full potential. While specific formats may vary, most comprehensive schedules incorporate the following key elements:

- Payment Number: A sequential identifier denoting each payment within the loan’s term. This provides a chronological record of the repayment process.

- Payment Date: Specifies the precise date on which each payment is due, aligning with the agreed-upon repayment schedule.

- Beginning Balance: The outstanding loan principal at the start of each payment period. This represents the debt that remains before the current payment is applied.

- Payment Amount: The fixed amount due for each payment period, encompassing both principal and interest. In many loan structures, this remains consistent throughout the loan’s duration.

- Principal Payment: The portion of the payment that directly reduces the outstanding loan balance. Early payments typically allocate a smaller percentage to principal.

- Interest Payment: The portion of the payment that covers the cost of borrowing, i.e., the lender’s compensation for providing the loan. This constitutes a larger share of early payments.

- Ending Balance: The remaining loan principal after the current payment is applied. This figure represents the continuously diminishing debt as the loan progresses.

- Cumulative Interest: An optional, but valuable, column that tracks the total interest paid over the life of the loan. This provides a holistic view of the cost of borrowing.

The Utility of Amortization Schedules: A Multifaceted Tool

Amortization schedules are far more than mere bookkeeping exercises; they serve a plethora of critical functions for both borrowers and lenders:

- Budgeting and Financial Planning: Borrowers can use the schedule to predict future loan payments, facilitating accurate budgeting and informed financial planning. This allows for anticipation of upcoming financial obligations.

- Debt Management: By visualizing the reduction of principal over time, borrowers can gain a deeper understanding of their debt and strategically manage their repayment strategy. This empowers borrowers to make informed decisions regarding accelerated payments or refinancing.

- Tax Purposes: The schedule provides a clear record of interest payments, which are often tax-deductible. This simplifies tax preparation and ensures accurate reporting.

- Loan Comparison: Amortization schedules allow for side-by-side comparison of different loan offers, revealing the true cost of borrowing by considering both interest rates and repayment terms.

- Financial Modeling: Lenders utilize amortization schedules for financial modeling, forecasting cash flows, and assessing the risk associated with lending. This underpins their pricing strategies and lending decisions.

- Accounting and Reporting: Businesses use amortization schedules for accurate accounting and financial reporting, ensuring compliance with regulatory standards. This is vital for transparent and reliable financial statements.

Illustrative Example: A Concrete Scenario

Imagine securing a mortgage of $200,000 at an annual interest rate of 5%, with a loan term of 30 years (360 months). An amortization schedule would meticulously outline each of the 360 monthly payments, demonstrating how a portion of each payment reduces the principal while the remainder covers the accrued interest. In the initial months, a larger proportion of the payment would be allocated to interest, gradually shifting toward principal reduction as the loan matures. By visualizing this process, the borrower can clearly see the trajectory of their debt repayment.

Beyond Simple Loans: Expanding the Scope of Amortization

While commonly associated with mortgages and personal loans, the principles of amortization extend to other financial contexts. For instance, the amortization of intangible assets, such as patents or copyrights, follows a similar principle of gradually expensing the asset’s value over its useful life. This allows for a systematic allocation of costs in accordance with accounting standards. The concept also applies to bond premiums and discounts, where the premium or discount is amortized over the life of the bond, affecting the bond’s yield.

Caveats and Considerations: A Word of Caution

While powerful, amortization schedules are not without limitations. They typically assume a fixed interest rate and consistent payment schedule. Variations in interest rates (as with adjustable-rate mortgages) or the implementation of extra principal payments will necessitate recalculation of the schedule. It is also important to remember that an amortization schedule is a projection, not a guarantee. Unexpected financial hardship can disrupt the repayment plan, altering the actual amortization trajectory.

In conclusion, an amortization schedule is an indispensable tool for navigating the complexities of debt repayment. It provides transparency, facilitates informed decision-making, and empowers both borrowers and lenders to effectively manage their financial obligations. The seemingly simple table holds a wealth of information, revealing the true cost of borrowing and charting a course toward financial solvency. Its enduring appeal lies not just in the numbers, but in the peace of mind it offers, knowing exactly where you stand on the path to debt freedom.