Ever stared at your bank statement, a cold dread washing over you as you see a mysterious charge labeled “Overdraft Fee?” It’s a common experience, and for many, it’s a painful reminder of the precarious tightrope they walk, balancing finances just to make ends meet. But what if you could mitigate this financial stumble? Enter overdraft protection, a seemingly benevolent offering from your bank. But is it truly a safety net, or just another revenue stream cleverly disguised? Let’s delve into the intricate world of overdraft protection, dissecting its mechanisms, weighing its pros and cons, and ultimately, helping you decide if it’s the right financial instrument for your individual circumstances.

Understanding the Labyrinth of Overdraft Protection

At its core, overdraft protection is a service offered by banks and credit unions designed to prevent your transactions from being declined when you don’t have sufficient funds in your account. Think of it as a financial stopgap, preventing the embarrassment and inconvenience of a bounced check or a rejected debit card purchase. It kicks in when you attempt to make a payment that exceeds your available balance. But how does it actually work? There are typically a few distinct flavors of overdraft protection.

Linked Account Transfer: This is often the simplest and most cost-effective option. Your checking account is linked to another account, such as a savings account or a credit card. When you overdraw, the bank automatically transfers funds from the linked account to cover the shortfall. This usually incurs a small transfer fee, which is significantly less than a standard overdraft fee.

Overdraft Line of Credit: This functions much like a traditional line of credit. The bank extends you a specific credit limit that you can draw upon to cover overdrafts. Interest is charged on the amount borrowed, similar to a credit card. This option provides more flexibility but can also be more expensive if not managed carefully.

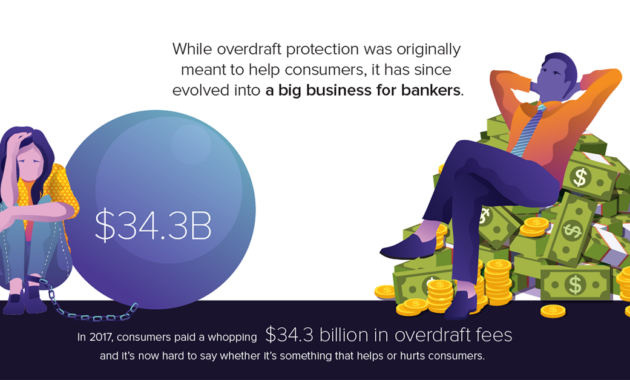

Standard Overdraft Coverage (Courtesy Overdraft): This is the most common, and often the most expensive, form of overdraft protection. The bank, at its discretion, will cover your overdraft, allowing the transaction to go through. However, this “courtesy” comes at a steep price – a hefty overdraft fee charged for each transaction covered. The potential for multiple fees in a single day can quickly escalate, turning a minor shortfall into a major financial burden.

The Siren Song of Convenience: Weighing the Pros

Overdraft protection, at first glance, appears to offer several compelling advantages. First, it provides peace of mind. Knowing that you won’t face the immediate repercussions of a declined transaction can be a significant stress reliever, especially when managing fluctuating income or unexpected expenses. Imagine being at the grocery store with a cart full of essentials, only to have your debit card rejected. Overdraft protection can prevent such an embarrassing and inconvenient scenario. Furthermore, it helps maintain a positive payment history. Avoiding bounced checks or declined payments can protect your credit score and prevent late payment fees from other creditors.

Navigating the Perils: Examining the Cons

Despite the apparent benefits, overdraft protection harbors significant drawbacks that warrant careful consideration. The most glaring issue is the cost. Standard overdraft fees can be exorbitant, often exceeding $30 per transaction. These fees can quickly accumulate, particularly if you frequently overdraw your account. For individuals living paycheck to paycheck, these fees can exacerbate financial instability, trapping them in a cycle of debt. Consider a scenario where you overdraw your account by a mere five dollars. The bank, in its “generosity,” covers the overdraft and slaps you with a $35 fee. That’s an effective interest rate that would make even the most predatory payday lender blush. Furthermore, overdraft protection can mask underlying financial problems. By allowing you to spend beyond your means, it can discourage responsible budgeting and financial planning. It’s akin to treating the symptom rather than addressing the root cause of the ailment.

Deciphering the Fine Print: Questions to Ask Your Bank

Before enrolling in any overdraft protection program, it’s crucial to thoroughly understand the terms and conditions. Inquire about the fee structure. How much is charged per overdraft transaction? Is there a daily limit on the number of overdraft fees you can incur? Also, understand the coverage limits. How much will the bank cover in overdrafts? Are there any restrictions on the types of transactions that are covered? Finally, explore alternative options. Are there lower-cost alternatives available, such as linking your account to a savings account or applying for an overdraft line of credit?

Beyond Overdraft Protection: Cultivating Financial Wellness

While overdraft protection can provide a temporary safety net, it’s essential to prioritize long-term financial wellness. Develop a detailed budget. Track your income and expenses to identify areas where you can cut back and save. Set up automatic transfers to your savings account. Even small, consistent contributions can add up over time. Consider using budgeting apps and tools. These apps can help you track your spending, set financial goals, and identify potential overdraft triggers. Monitor your account balance regularly. Stay informed about your available funds to avoid unintentional overdrafts. And, consider setting up low-balance alerts. Many banks offer alerts that notify you when your account balance falls below a certain threshold, giving you time to transfer funds or adjust your spending habits.

The Verdict: Is Overdraft Protection Worth It?

The answer, as with most financial questions, is nuanced and depends entirely on your individual circumstances. For some, overdraft protection can provide valuable peace of mind and prevent costly mistakes. However, for others, it can be a costly trap that exacerbates financial instability. If you consistently overdraw your account, overdraft protection is likely not the solution. Instead, focus on improving your budgeting skills and financial habits. If you rarely overdraw your account but want a safety net for occasional emergencies, a linked account transfer may be a reasonable option. Ultimately, the decision of whether or not to enroll in overdraft protection requires careful consideration of your financial habits, risk tolerance, and the specific terms and conditions of the program. Remember, financial wellness is a journey, not a destination. Take the time to educate yourself, explore your options, and make informed decisions that align with your long-term financial goals.