The concept of collateral in loan agreements, while seemingly straightforward, often piques the curiosity of borrowers and lenders alike. It’s more than just a safeguard; it represents a fundamental aspect of risk management and a tangible link between the lender’s confidence and the borrower’s commitment. What exactly constitutes collateral, and why is it so crucial to the lending process? This exploration delves into the intricacies of collateral, unraveling its significance in the financial landscape.

Defining Collateral: A Foundation of Secured Lending

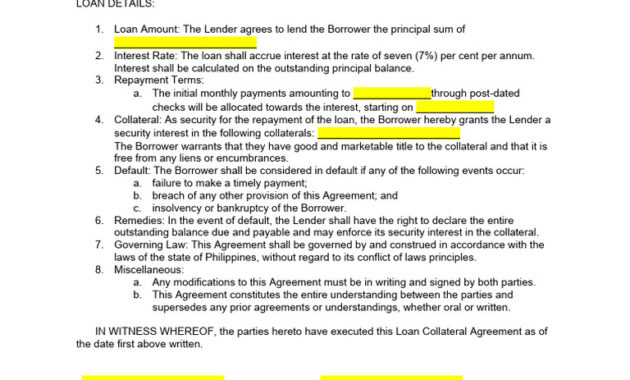

At its core, collateral is an asset pledged by a borrower to a lender as security for a loan. This asset serves as a contingent repayment source if the borrower defaults on their loan obligations. It’s a tangible assurance, transforming a potentially unsecured loan into a secured one, thereby mitigating the lender’s risk exposure. The type of asset accepted as collateral can vary widely, depending on the loan amount, the borrower’s financial standing, and the lender’s risk tolerance. These can include real estate, vehicles, equipment, inventory, securities (stocks and bonds), accounts receivable, and even intellectual property.

The Multifaceted Role of Collateral

Collateral serves a dual purpose. Firstly, it provides the lender with a recourse mechanism in the event of default. If the borrower fails to repay the loan as agreed, the lender has the legal right to seize the collateral, sell it, and use the proceeds to recover the outstanding debt. This right of repossession and liquidation is paramount in protecting the lender’s financial interests. Secondly, collateral incentivizes the borrower to diligently fulfill their repayment obligations. The potential loss of a valuable asset serves as a strong deterrent against default, encouraging responsible financial behavior and proactive debt management.

Types of Collateral: A Diverse Landscape of Assets

The selection of appropriate collateral hinges on several factors, including its liquidity, marketability, and stability of value. Let’s examine some common types of collateral:

- Real Estate: Homes, land, and commercial properties are frequently used as collateral due to their relatively stable value and established market. Mortgages, for example, are secured loans using real estate as collateral. The lender holds a lien on the property, giving them the right to foreclose if the borrower defaults.

- Vehicles: Cars, trucks, and other vehicles can serve as collateral for auto loans. The lender retains a security interest in the vehicle until the loan is fully repaid. The vehicle’s resale value is a key consideration in determining its suitability as collateral.

- Equipment: Businesses often use equipment, such as machinery, computers, and manufacturing tools, as collateral for loans to finance their operations. The equipment’s useful life and resale value are crucial factors.

- Inventory: Retail businesses may pledge their inventory as collateral for working capital loans. The lender assesses the inventory’s marketability and storage costs when evaluating its suitability.

- Securities: Stocks, bonds, and other financial instruments can be used as collateral. The lender typically requires the borrower to maintain a certain margin of equity to protect against market fluctuations.

- Accounts Receivable: Businesses can use their accounts receivable (money owed by customers) as collateral. The lender evaluates the creditworthiness of the business’s customers to assess the risk.

- Cash: Cash or cash equivalents, such as certificates of deposit (CDs), are considered highly liquid and secure forms of collateral.

- Intellectual Property: Patents, trademarks, and copyrights can serve as collateral, particularly for technology-based companies. Valuing intellectual property can be complex, requiring expert appraisals.

The Loan-to-Value Ratio (LTV): A Key Metric

The loan-to-value (LTV) ratio is a critical metric in secured lending. It represents the loan amount as a percentage of the collateral’s appraised value. A lower LTV ratio indicates a greater equity cushion for the lender, reducing their risk. For instance, a loan with an LTV of 80% means that the loan amount is 80% of the collateral’s value, leaving a 20% equity buffer. Lenders carefully consider the LTV ratio when approving secured loans, often setting maximum LTV limits based on the type of collateral and the borrower’s creditworthiness. This ratio is a cornerstone of risk assessment, ensuring the lender has sufficient recourse in case of default.

The Legal Framework: Security Agreements and Liens

The use of collateral is governed by a robust legal framework. A security agreement is a contract that outlines the terms and conditions of the loan, including the specific collateral pledged, the borrower’s obligations, and the lender’s rights. This agreement is typically filed with a relevant government agency to create a public record of the lender’s security interest. This public record establishes a lien on the collateral, giving the lender priority over other creditors in the event of default. The Uniform Commercial Code (UCC) provides a standardized set of rules for secured transactions, ensuring consistency and predictability across jurisdictions. Understanding these legal nuances is vital for both borrowers and lenders to protect their respective interests.

Appraisal and Valuation: Determining Collateral Worth

Accurately determining the value of collateral is paramount to the lending process. Lenders typically require an independent appraisal to assess the fair market value of the asset. The appraisal process involves a thorough inspection, analysis of comparable sales, and consideration of market conditions. For certain types of collateral, such as securities, the value can fluctuate rapidly, requiring ongoing monitoring and adjustments. The appraisal provides the lender with a reliable estimate of the collateral’s worth, enabling them to make informed lending decisions and manage their risk effectively. The valuation process is not static; it requires periodic updates to reflect changes in market dynamics and asset depreciation.

Risks and Considerations: Navigating the Collateral Landscape

While collateral provides significant security, it’s not without its limitations. The value of collateral can decline due to market fluctuations, economic downturns, or physical damage. The lender may incur expenses in seizing, maintaining, and selling the collateral in the event of default. Furthermore, legal disputes can arise regarding the validity of the security agreement or the priority of the lender’s lien. Borrowers should carefully consider the implications of pledging their assets as collateral, weighing the benefits of securing a loan against the risk of potential loss. Lenders, conversely, need to conduct thorough due diligence to assess the collateral’s true value and potential risks.

Collateral: A Cornerstone of Financial Stability

In conclusion, collateral serves as a fundamental pillar of secured lending, fostering financial stability and promoting responsible borrowing practices. It bridges the gap between lender confidence and borrower commitment, enabling access to credit for individuals and businesses. The diverse types of collateral, the legal framework governing its use, and the valuation methods employed all contribute to its effectiveness as a risk mitigation tool. While risks and considerations exist, the strategic use of collateral remains a cornerstone of the financial landscape, supporting economic growth and facilitating access to capital. The intricacies of collateral, therefore, are not merely academic; they are essential to understanding the dynamics of modern finance.

This detailed exploration sheds light on the crucial role collateral plays in securing loans and managing financial risk. Beyond serving as mere security, collateral embodies a dynamic relationship between lenders and borrowers, balancing protection with accountability. The variety of acceptable collateral assets-from real estate to intellectual property-reflects the diverse needs across lending scenarios and industries. Understanding the loan-to-value ratio and the underlying legal framework highlights how lenders safeguard their interests while enabling borrowers to access necessary capital. Yet, the potential risks involved, such as asset depreciation and legal complexities, remind borrowers to carefully evaluate their commitments. Overall, this comprehensive overview emphasizes collateral’s central place in facilitating responsible lending and economic stability, underscoring why it remains a foundational element in modern financial systems.

Joaquimma-Anna’s in-depth examination of collateral effectively demystifies its multifaceted role within loan agreements. By articulating collateral not only as a security but also as a vital risk management tool, the article highlights how it strengthens lender confidence while reinforcing borrower responsibility. The detailed breakdown of asset types-from traditional real estate to more nuanced intellectual property-illustrates the adaptability of collateral to diverse lending needs. Emphasizing key concepts like the loan-to-value ratio and security agreements further clarifies how legal frameworks and valuation practices protect all parties involved. Importantly, acknowledging the risks such as value depreciation and potential legal challenges provides a balanced perspective. This comprehensive analysis reinforces collateral’s indispensable position in securing credit, promoting financial prudence, and sustaining economic growth.

Joaquimma-Anna’s thorough analysis of collateral offers an insightful perspective on its pivotal role in the lending ecosystem. By framing collateral not just as a security mechanism but as a critical intersection between risk management and borrower accountability, the article deepens our understanding of secured loans. Highlighting diverse collateral types, from tangible assets like real estate and equipment to intangible ones such as intellectual property, underscores the flexibility and evolving nature of lending practices. The emphasis on the loan-to-value ratio and the importance of legal safeguards like security agreements elucidates how lenders maintain protection while facilitating credit access. Moreover, addressing risks such as valuation challenges and potential legal disputes provides a realistic, balanced view. This comprehensive breakdown reinforces collateral’s essential function in fostering financial stability and enabling prudent borrowing decisions within today’s complex financial landscape.