Ever ponder how the labyrinthine world of healthcare finance metamorphosed post-Affordable Care Act (ACA)? It’s a legitimate query, especially when navigating the intricacies of premiums, deductibles, and cost-sharing arrangements. The ACA, enacted in 2010, sought to overhaul the American healthcare system, and its ripple effects on financing are still being felt. Did the financial burden on families truly alleviate, or did it merely shift its weight? Let’s delve into the seismic shifts the ACA triggered in the healthcare financing landscape.

I. Expanding the Insurance Net: A Paradigm Shift

The ACA’s cornerstone was expanding health insurance coverage. Prior to its enactment, millions of Americans lacked access to health insurance, leaving them vulnerable to financial ruin in the event of illness or injury. The ACA addressed this lacuna through several key mechanisms:

A. Medicaid Expansion: Broadening Eligibility Criteria

One of the most significant provisions was the expansion of Medicaid eligibility. States were incentivized to extend coverage to individuals with incomes up to 138% of the federal poverty level. This initiative aimed to provide a safety net for low-income individuals and families who previously fell through the cracks. However, the Supreme Court ruling made Medicaid expansion optional for states, resulting in a patchwork of coverage across the nation. States that embraced expansion witnessed a dramatic reduction in their uninsured rates, while those that resisted continued to grapple with higher numbers of uninsured residents. The fiscal implications for both the federal government and participating states were considerable, requiring careful budgetary management.

B. Health Insurance Marketplaces: A New Arena for Individual Coverage

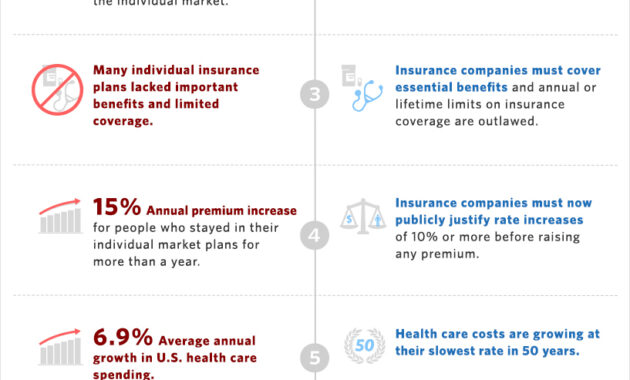

The ACA established Health Insurance Marketplaces, also known as exchanges, where individuals and small businesses could purchase health insurance plans. These marketplaces offered a standardized platform for comparing plans and accessing premium subsidies. Premium subsidies, in the form of advance premium tax credits (APTCs), were made available to eligible individuals and families with incomes between 100% and 400% of the federal poverty level. These subsidies helped to make coverage more affordable, enabling more people to enroll in health insurance. The Marketplaces also mandated that all plans offered meet certain minimum standards, ensuring that consumers had access to comprehensive coverage.

C. Employer Mandate: Incentivizing Employer-Sponsored Coverage

The ACA included an employer mandate, requiring employers with 50 or more full-time employees to offer health insurance coverage to their employees or face penalties. This provision aimed to encourage employers to maintain or expand their employer-sponsored coverage, which remains the primary source of health insurance for many Americans. The employer mandate has had a complex impact, with some employers choosing to offer coverage, while others have opted to pay the penalty. The effect on employment rates has been a subject of ongoing debate among economists.

II. Altering the Financial Landscape: Subsidies, Taxes, and Payment Reforms

The ACA not only expanded coverage but also transformed the financial structure of the healthcare system. This involved implementing new subsidies, taxes, and payment reforms designed to improve efficiency and control costs.

A. Premium Subsidies and Cost-Sharing Reductions: Alleviating the Financial Burden

As mentioned previously, the ACA provided premium subsidies to eligible individuals and families purchasing coverage through the Health Insurance Marketplaces. In addition, cost-sharing reductions (CSRs) were available to those with incomes below 250% of the federal poverty level. CSRs helped to lower out-of-pocket costs, such as deductibles, copayments, and coinsurance, making healthcare more affordable for low-income individuals. However, the Trump administration’s decision to discontinue CSR payments to insurers created instability in the Marketplaces, leading to higher premiums for many consumers. This policy shift underscored the political vulnerability of the ACA’s financial architecture.

B. New Taxes: Funding the Expansion of Coverage

The ACA was financed in part by new taxes, including a tax on high-cost employer-sponsored health plans (the “Cadillac tax,” although it was repealed before taking effect), taxes on medical devices and pharmaceutical companies, and an increase in the Medicare payroll tax for high-income earners. These taxes were designed to generate revenue to offset the costs of expanding coverage and improving healthcare quality. The economic impact of these taxes has been a subject of debate, with some arguing that they could harm certain sectors of the economy.

C. Payment Reforms: Shifting from Volume to Value

The ACA promoted payment reforms aimed at shifting the healthcare system from a fee-for-service model, which incentivizes volume, to a value-based care model, which rewards quality and efficiency. These reforms included the creation of Accountable Care Organizations (ACOs), which are groups of doctors, hospitals, and other healthcare providers who work together to provide coordinated, high-quality care to their patients. The ACA also incentivized the adoption of bundled payments, which provide a single payment for an episode of care, encouraging providers to deliver care more efficiently. The effectiveness of these payment reforms in controlling costs and improving quality is still being evaluated.

III. Ongoing Debates and Future Directions

The ACA has been a subject of intense political debate since its enactment, and its future remains uncertain. Ongoing debates revolve around issues such as the affordability of premiums, the stability of the Health Insurance Marketplaces, and the role of government in healthcare. Proposals to repeal or replace the ACA have been introduced in Congress, but none have succeeded to date. The future of healthcare financing in the United States will depend on the outcome of these ongoing debates and the policy choices made by future administrations.

The Act brought about undeniable changes in healthcare financing, expanding coverage and introducing new financial mechanisms. While questions about affordability and sustainability persist, the ACA’s legacy as a watershed moment in American healthcare history is secure. Its effects will continue to reverberate through the system for years to come, shaping the financial landscape of healthcare and impacting the lives of millions of Americans. The quest for a more equitable and efficient healthcare system remains an ongoing challenge, requiring continuous evaluation and adaptation.