Quick Answer

A crossed cheque is a payment instrument marked with two parallel lines, restricting it to bank deposit only and preventing direct cash withdrawal. This enhances security, traceability, and accountability in financial transactions.

Infobox: Crossed Cheque at a Glance

| Feature | Description |

|---|---|

| Definition | A cheque marked with two parallel lines restricting payment method |

| Purpose | To ensure cheque is deposited into a bank account only |

| Security | Prevents cashing over the counter, reducing fraud risk |

| Usage | Common in secure and traceable financial transactions |

| Types of Cheques Related | Bearer cheque, order cheque |

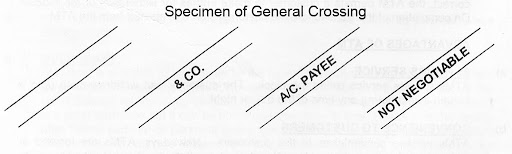

Overview of Crossed Cheques

In financial transactions, a cheque serves as a negotiable instrument directing a bank to pay a specified amount from the drawer’s account to the payee. Among its various forms, the crossed cheque stands out by incorporating a security feature: two parallel lines drawn across its face. This marking transforms the cheque’s negotiability by mandating that it be deposited directly into a bank account rather than cashed immediately at the bank counter.

How Crossing a Cheque Changes Its Handling

The act of crossing a cheque imposes a critical restriction on its payment method. Unlike an uncrossed cheque, which can be encashed over the counter, a crossed cheque must be credited to a bank account. This procedural change fosters a more secure and accountable payment process by creating a verifiable transaction trail within the banking system.

Why Crossing a Cheque Matters

Crossing a cheque is more than a mere formality; it is a deliberate measure to enhance the security and integrity of financial dealings. By limiting payment to bank deposits, it reduces the risk of theft or fraud and ensures that funds are traceable. This mechanism builds trust between the issuer and the recipient, as the cheque’s path through the banking network provides transparency and accountability.

Common Misunderstandings About Crossed Cheques

One frequent misconception is that crossing a cheque makes it non-negotiable. In reality, a crossed cheque remains negotiable but with the condition that it must be deposited into a bank account. Another myth is that crossing guarantees absolute fraud prevention; while it significantly reduces risk, it does not eliminate all possibilities of misuse.

Example of a Crossed Cheque in Practice

Consider a business paying a supplier via cheque. By crossing the cheque, the business ensures the supplier cannot immediately cash it at the bank counter, but must deposit it into their bank account. This process creates a clear record of payment, protecting both parties and facilitating easier reconciliation of accounts.

Related Terms

- Bearer Cheque: Payable to the person holding the cheque, can be cashed immediately.

- Order Cheque: Payable to a specified person or their order, can be endorsed.

- Negotiable Instrument: A document guaranteeing payment of a specific amount.

Frequently Asked Questions (FAQ)

Can a crossed cheque be cashed directly?

No, a crossed cheque must be deposited into a bank account and cannot be cashed over the counter.

What do the two parallel lines on a cheque signify?

They indicate that the cheque is crossed and restrict payment to bank deposit only.

Does crossing a cheque prevent all types of fraud?

While it greatly reduces the risk by ensuring traceability, it does not completely eliminate the possibility of fraud.

Can a crossed cheque be transferred to another person?

Yes, but it must be deposited into the bank account of the payee or their endorsed party.

Final Answer

A crossed cheque is a secure financial instrument marked by two parallel lines, which restricts payment to bank deposits only. This feature enhances transaction security, promotes transparency, and helps prevent fraud, making it a preferred choice for responsible financial exchanges.

References

- Reserve Bank of India. (n.d.). Cheques and Crossing. Retrieved from https://rbi.org.in

- Investopedia. (n.d.). Crossed Cheque Definition. Retrieved from https://www.investopedia.com

- Financial Dictionary. (n.d.). Negotiable Instruments. Retrieved from https://financial-dictionary.com

Edward Philips offers a compelling exploration of crossed cheques, highlighting their role as more than just a payment method but as a symbol of security and trust in financial transactions. The deliberate act of crossing a cheque imposes critical restrictions that promote transparency by ensuring funds are traceable through banking channels. This not only protects the issuer’s assets but also instills confidence in the payee, fostering accountability and deterring fraud. Beyond technicalities, the crossed cheque reflects a broader philosophy emphasizing responsible monetary exchanges in an era often dominated by convenience over caution. By understanding crossed cheques alongside bearer and order cheques, learners gain deeper insight into the evolving nature of negotiable instruments and the essential principles that govern trustworthy commerce. This nuanced approach enriches financial literacy and underscores the vital intersection of security and integrity in payment systems.

Edward Philips’ detailed analysis eloquently unpacks the layered significance of crossed cheques, positioning them as pivotal tools that balance security with trust in the realm of negotiable instruments. The discussion reveals how crossing a cheque transforms a simple payment method into a safeguard that ensures funds are securely routed through banking institutions, thereby reducing the risk of fraud and enhancing transaction traceability. This act embodies a conscious shift toward accountability and financial responsibility, reinforcing the importance of deliberate controls in an increasingly complex economic environment. Moreover, Edward’s insights invite readers to broaden their understanding beyond crossed cheques, encouraging exploration of other forms like bearer and order cheques, which each carry distinct implications for risk and control. Ultimately, this thoughtful exposition underscores the vital role of such instruments in fostering integrity and transparency, core tenets that underpin sound financial dealings.

Edward Philips’ comprehensive exploration of crossed cheques brilliantly elucidates how a seemingly simple payment instrument can be transformed into a sophisticated mechanism for ensuring security and trust. By imposing restrictions through the crossing, issuers effectively channel payments exclusively through banking systems, greatly reducing vulnerabilities such as fraud and unauthorized encashment. This constraint not only safeguards financial interests but also fosters transparency and traceability, critical components for maintaining accountability in modern financial transactions. Moreover, Edward’s discussion thoughtfully places crossed cheques within the broader spectrum of negotiable instruments, inviting readers to appreciate the diversity and intentional design behind different cheque types. His analysis deftly highlights how crossing is not just a procedural formality but a deliberate assertion of control and mutual trust, essential values in today’s intricate economic landscape. This commentary significantly enhances our understanding of how traditional financial tools adapt to uphold integrity and responsibility.

Edward Philips’ article provides an insightful and nuanced perspective on the crossed cheque, elevating it beyond a mere financial instrument into a deliberate mechanism for securing transactions and fostering trust. By emphasizing the intentional restriction of payment methods through crossing, the piece highlights how this practice protects both the issuer and payee by channeling funds exclusively through banking systems. This restriction intricately ties into broader themes of transparency and accountability, vital in deterring fraud and ensuring transaction traceability. Additionally, Edward’s exploration of crossed cheques as a reflection of a mindful approach to financial responsibility encourages readers to appreciate the thoughtful design behind various payment instruments. His work importantly bridges traditional cheque practices with modern demands for security, illustrating how such seemingly simple tools remain relevant in cultivating integrity within today’s complex financial frameworks.

Edward Philips’ article masterfully elevates the crossed cheque from a simple payment method to a profound instrument of financial integrity. By highlighting how crossing mandates banking-channel transactions, Edward underscores the importance of control, security, and transparency in today’s financial ecosystem. This deliberate restriction not only mitigates fraud risk but reinforces trust between parties, transforming a routine financial practice into a meaningful assurance of accountability. His exploration also invites reflection on the evolving nature of negotiable instruments, urging readers to appreciate the thoughtful mechanisms designed to safeguard transactions amid complex economic realities. Ultimately, Edward’s insights remind us that crossed cheques embody more than procedure-they represent a thoughtful commitment to responsible and secure financial exchanges.

Edward Philips’ examination of crossed cheques offers a profound insight into how a simple endorsement on a negotiable instrument fundamentally reshapes the payment landscape. By mandating that such cheques be deposited only through banking channels, crossing enhances both security and transparency, crucial in today’s increasingly digitized and fraud-prone financial environment. This act demonstrates an intentional assertion of control that benefits all parties by ensuring traceability and reducing the likelihood of misuse. Beyond the practical safeguard, Philips eloquently frames crossing as a symbol of trust and accountability, inviting deeper reflection on how traditional tools evolve to meet modern demands. His nuanced exploration not only clarifies the operational mechanics but also elevates crossed cheques as a testament to responsible financial stewardship and integrity.

Edward Philips’ reflective analysis of crossed cheques beautifully captures their critical role in enhancing security and trust within financial transactions. By deliberately restricting payment to banking channels, crossing a cheque mitigates risks like fraud and misuse, offering both issuers and recipients reassurance through transparency and accountability. This nuanced control mechanism transforms a routine financial act into a deliberate practice of responsible stewardship, emphasizing the importance of traceability in today’s complex economic landscape. Furthermore, Philips’ discussion encourages deeper consideration of the diverse forms and functions of negotiable instruments, such as bearer and order cheques, highlighting the evolving interplay between tradition and modern financial safeguards. Overall, his exploration elevates the crossed cheque beyond a mere procedural tool, framing it as a meaningful commitment to integrity and prudent financial management.

Edward Philips’ detailed examination of crossed cheques compellingly underscores their role as more than mere financial instruments-they are pivotal tools fostering security, trust, and accountability in payment transactions. By mandating deposit through banking channels only, the crossing effectively enforces a safeguarded pathway that diminishes fraud risks and ensures comprehensive traceability. This nuanced act embodies a deliberate assertion of control by the issuer, reinforcing mutual confidence between payer and payee. Additionally, Philips’ insights invite a broader reflection on the evolution of negotiable instruments, illustrating how traditional practices adapt to contemporary demands for transparency and financial integrity. His analysis elevates the crossed cheque into a meaningful symbol of responsible stewardship, reminding us that in the complex financial ecosystem, the interplay of tradition and innovation remains vital to upholding the principles of trust and security.

Edward Philips’ comprehensive analysis of crossed cheques aptly illustrates how a simple yet deliberate act reshapes financial transactions by embedding security and accountability at their core. Crossing a cheque is much more than a technical formality; it serves as a protective mechanism that channels payments exclusively through banking systems, thereby fostering transparency and traceability. Philips thoughtfully captures how this practice not only reduces fraud risks but also symbolizes an implicit bond of trust between the issuer and payee. His insights further invite a deeper appreciation of negotiable instruments’ evolving roles in balancing convenience with caution. In today’s intricate financial landscape, the crossed cheque stands as a testament to responsible stewardship, reminding us that safeguarding monetary exchanges requires both tradition and mindful innovation working hand in hand.

Edward Philips’ insightful discourse on crossed cheques brilliantly encapsulates their pivotal role as instruments of financial prudence and trust. By delineating how the act of crossing transforms a cheque into a secure, traceable payment directive strictly channeled through banks, he highlights an often-overlooked layer of transactional integrity. This mechanism acts as a safeguard against fraud while reinforcing mutual accountability between issuers and recipients. Philips’ exploration extends beyond procedural nuances to reveal the philosophical underpinnings of control and responsibility embedded within crossed cheques. His reflection on their evolution alongside related negotiable instruments invites readers to appreciate the dynamic balance between tradition and innovation in safeguarding financial dealings. Ultimately, this piece serves as a timely reminder that even simple instruments, when thoughtfully employed, can uphold foundational principles of trust and security in an increasingly complex economic landscape.

Edward Philips’ comprehensive exploration of crossed cheques eloquently highlights how this simple yet deliberate act significantly fortifies financial transactions by embedding control, security, and transparency into everyday banking practices. Crossing a cheque effectively transforms it from a negotiable instrument payable to bearer or order, into a directive that channels payments exclusively through trusted banking institutions. This restriction mitigates risks of fraud and misuse while fostering a clear, auditable trail that benefits issuers and recipients alike. Beyond mere procedural formality, Philips thoughtfully reveals the crossed cheque as a profound statement of responsible finance-an enduring symbol of trust and accountability in an evolving economic landscape. His analysis enriches contemporary understanding by positioning crossed cheques not only as protective tools but as embodiments of prudent stewardship and financial integrity.

Edward Philips’ intricate analysis of crossed cheques delves deeply into their vital role as instruments that enhance both security and accountability within financial transactions. By restricting payment to bank deposits, the crossing mechanism effectively minimizes risks of fraud and unauthorized cashing, thereby fostering a secure and traceable payment process. Philips thoughtfully frames this practice not just as a procedural formality but as a conscious assertion of control that reinforces trust between the issuer and the recipient. His exploration also invites reflection on the broader evolution of negotiable instruments, illustrating how traditional financial tools adapt to modern demands for transparency and responsibility. Ultimately, this discussion underscores the crossed cheque as a symbolic and practical commitment to integrity, prudent stewardship, and the careful balance between convenience and financial security in today’s complex economic environment.

Edward Philips’ exposition on crossed cheques offers a rich, multidimensional perspective that highlights their critical function in promoting secure and accountable financial transactions. By emphasizing the intentional restriction of payment methods through the act of crossing, Philips effectively presents the cheque as a controlled instrument that mitigates fraud and fosters transparency. This focused approach underscores how seemingly simple practices embed deeper values of trust and responsibility within everyday banking. Additionally, his exploration of crossed cheques invites further inquiry into the evolution of negotiable instruments, revealing an ongoing dialogue between tradition and modern financial prudence. Ultimately, Philips elevates the crossed cheque beyond a mere procedural tool, portraying it as a powerful affirmation of integrity and thoughtful stewardship in navigating today’s intricate economic landscape.

Edward Philips’ detailed exposition on crossed cheques offers a profound insight into the deliberate safeguards embedded within traditional financial instruments. By emphasizing the intentional crossing, he highlights how this act transforms a commonplace cheque into a secure, traceable transaction tool that channels payments exclusively through banking institutions. This not only mitigates fraud but reinforces mutual trust and accountability between the issuer and recipient. Philips’ analysis skillfully connects procedural formalities with the broader principles of financial integrity, underscoring the crossed cheque as a symbol of conscientious stewardship in an increasingly complex economic environment. His work encourages reflection on the evolving nature of negotiable instruments and invites a thoughtful balance between convenience, security, and transparency in modern financial practices.

Edward Philips’ examination of crossed cheques offers a compelling insight into how a seemingly simple financial instrument can embody complex principles of security and trust. By imposing restrictions on payment methods, crossing a cheque transforms it into a tool that ensures funds are traceable and protected against misuse. This deliberate act not only safeguards the issuer’s resources but also reinforces confidence for the recipient, enabling a clearer audit trail within the banking system. Philips’ discussion elevates the crossed cheque from a mere procedural convention to a meaningful expression of financial responsibility and integrity. In highlighting this nuanced practice, the commentary invites a broader reflection on how traditional instruments adapt to contemporary demands for transparency and accountability, reminding us that thoughtful design in payment methods remains vital amidst evolving economic complexities.

Edward Philips’ insightful discourse on crossed cheques adeptly illuminates how this nuanced financial instrument serves as a critical safeguard in banking transactions. By enforcing payment exclusively through bank deposits, crossing a cheque introduces deliberate constraints that effectively enhance security and traceability, reducing opportunities for fraud. Philips’ perspective skillfully transcends the mere technicalities, portraying the crossed cheque as a tangible expression of trust and mutual responsibility between payer and payee. This controlled negotiation mechanism thereby promotes greater financial accountability and transparency in an era increasingly concerned with secure and auditable payment methods. Furthermore, his exploration encourages a deeper appreciation of traditional instruments’ adaptability amid evolving commercial demands, highlighting their ongoing relevance as tools for prudent financial stewardship and ethical transaction management.

Edward Philips’ comprehensive analysis of crossed cheques profoundly underscores their pivotal role in enhancing security and accountability in financial transactions. By mandating that payments be processed exclusively through bank accounts, crossed cheques serve as an effective barrier against misuse and fraud. Philips eloquently presents crossing not just as a technical detail but as a meaningful expression of trust and responsibility between issuer and payee. This intentional restriction transforms the cheque into a traceable, transparent instrument that aligns with contemporary demands for secure payment methods. Moreover, his reflection on the broader context of negotiable instruments highlights how traditional tools evolve to address the complexities of modern commerce, reinforcing the crossed cheque as both a practical safeguard and a symbol of conscious financial stewardship.

Edward Philips’ elucidation on crossed cheques profoundly captures the essence of this financial mechanism as more than just a functional restriction-it is a deliberate assertion of security and fiduciary prudence. By mandating that payments be routed solely through banking channels, the crossed cheque not only curtails potential financial malfeasance but also fortifies trust between the payer and payee, ensuring transparency and traceability. Philips’ reflection on this practice underscores the dynamic interplay between convenience and caution, highlighting how traditional instruments adapt to contemporary demands for integrity in financial dealings. His work encourages a deeper recognition of how such seemingly simple measures embed core principles of responsibility and accountability within the complex fabric of modern commerce. This insightful commentary enriches our understanding of negotiable instruments as evolving tools aligned with ethical financial stewardship.

Building upon Edward Philips’ thorough exploration and previous thoughtful reflections, it is clear that the crossed cheque represents far more than a simple banking formality. It acts as an essential instrument reinforcing transparency and accountability within financial transactions, which is increasingly critical in today’s fast-paced economic environment. By restricting payment exclusively to bank deposits, crossing a cheque minimizes risks associated with cash payments and instills confidence for both issuers and payees. This mechanism reflects a broader principle that financial tools must evolve to meet growing demands for security and traceability without sacrificing trust. Moreover, Philips’ insights encourage us to appreciate how nuanced features in payment instruments like crossing foster responsible financial behavior and uphold the integrity of commerce, blending tradition and modernity in promoting ethical stewardship of monetary exchanges.

Building on Edward Philips’ profound analysis, it becomes evident that the crossed cheque is much more than a procedural formality-it is a strategic instrument that fosters secure, accountable financial exchanges. The deliberate restriction to bank deposit payments mitigates risks inherent in cash transactions, thereby enhancing the integrity of the payment process. Philips’ emphasis on the moral and fiduciary dimensions of crossing a cheque enriches our understanding of how such instruments promote trust and transparent transaction trails. This practice reflects an intentional, thoughtful approach to managing financial risk, reminding us that even traditional mechanisms can evolve to meet the heightened demands for security in today’s complex economic environment. Ultimately, crossed cheques symbolize a commitment to ethical stewardship, reinforcing the foundational relationship between payer and payee through controlled and traceable payment flows.

Edward Philips’ thoughtfully articulated analysis underscores how a crossed cheque transcends its role as a mere procedural formality to embody a profound commitment to transactional security and ethical responsibility. The deliberate restriction to bank deposits curtails risks linked with cash handling, fostering a payment environment marked by transparency and traceability. This practice enriches our understanding of negotiable instruments as dynamic entities that adapt to contemporary financial challenges while upholding foundational trust between payer and payee. Philips’ emphasis on the implicit covenant established by crossing a cheque invites deeper reflection on how traditional financial tools can encourage mindful stewardship and accountability amid a rapidly evolving economic landscape. His insights powerfully remind us that even simple methods of payment can carry significant meaning in promoting secure, responsible financial interactions.

Building upon Edward Philips’ insightful exposition, the crossed cheque emerges as a vital financial mechanism that transcends its simple physical marking. It symbolizes a deliberate imposition of control designed to safeguard transactions by limiting payment methods to secure banking channels. This restriction effectively mitigates risks associated with cash transactions and reinforces the accountability of all parties involved. Philips’ reflections illuminate the crossed cheque as an embodiment of trust-an implicit agreement that encourages transparency and traceability, which are essential in today’s complex financial ecosystem. Furthermore, his discussion invites us to appreciate how such traditional instruments adapt thoughtfully to meet evolving security needs while fostering responsible financial behavior. In essence, the crossed cheque represents not only practical prudence but also an ethical commitment to maintaining integrity in monetary exchanges.

Expanding on Edward Philips’ insightful analysis, the crossed cheque embodies a strategic balance between convenience and security in financial transactions. By restricting payment exclusively to bank deposits, it enforces a traceable, transparent process that greatly diminishes the risks associated with cash payments, such as theft or fraud. This protective measure not only safeguards the funds of the issuer but also provides the recipient with a clear audit trail, fostering trust and confidence in the transaction. Beyond its procedural role, the crossed cheque serves as a reminder of the ethical responsibilities inherent in financial exchanges, advocating for prudent stewardship of resources in an increasingly complex economic landscape. Philips’ exploration reveals how such traditional instruments continue to evolve, aligning longstanding financial practices with modern demands for accountability and secure commerce.

Expanding on Edward Philips’ comprehensive examination, the crossed cheque emerges as a pivotal financial safeguard that elegantly combines tradition with contemporary concerns for security and transparency. By mandating deposit into a bank account, it constrains payment channels to those that inherently provide auditability and reduce exposure to risks such as theft or fraud. This restriction not only protects the issuer’s assets but also establishes a transparent payment trail, enhancing trust and accountability between parties. Philips’ insight into the ethical underpinnings of this practice highlights how seemingly simple procedural choices can carry profound implications for responsible financial conduct. In an era increasingly dominated by digital transactions, the crossed cheque serves as a reminder that robust financial instruments continue to evolve thoughtfully, encouraging integrity and confidence in monetary exchanges.

Edward Philips’ exploration of the crossed cheque compellingly underscores its role as both a protective financial instrument and a symbol of trustworthiness in monetary transactions. By effectively restricting the cheque to bank deposits only, crossing it not only reduces the risk of theft and fraud but also instills an essential layer of transparency through traceability. This action transforms the cheque into a testament of responsibility, enhancing confidence between the issuer and recipient by ensuring accountability. His nuanced analysis reminds us that even traditional instruments like cheques adapt to modern demands for security and integrity, reinforcing ethical financial conduct in an increasingly complex economic landscape. The crossed cheque, therefore, emerges as a bridge connecting procedural security with the deeper values of trust and conscientious stewardship in financial dealings.

Building upon Edward Philips’ comprehensive exploration, the crossed cheque stands out as more than a mere financial instrument-it is a deliberate assertion of control and security in payment processes. By restricting negotiation exclusively to bank deposits, the practice mitigates risks inherent in cash transactions such as theft, loss, or misuse, thereby enhancing both issuer and recipient confidence. Philips eloquently connects this procedural detail to broader themes of trust, responsibility, and transparency, highlighting how even traditional financial tools evolve to address modern concerns. The crossed cheque serves as a tangible reminder that safeguarding funds is not only a technical matter but also an ethical commitment to integrity and accountability in financial dealings. In a landscape increasingly oriented toward digital convenience, this instrument’s enduring relevance underscores the importance of balancing ease with conscientious stewardship.

Edward Philips’ detailed examination of the crossed cheque profoundly highlights its role as a layered instrument of financial control and security. By mandating that crossed cheques be deposited only into bank accounts, the issuer enforces a stricter framework that both deters fraud and enhances transactional traceability. This restriction transforms a straightforward payment method into a safeguard that cultivates trust and accountability between payer and payee. Philips’ insights bridge procedural nuances with broader ethical principles, revealing how even traditional instruments adapt to evolving economic complexities. The crossed cheque thus signifies more than a payment directive-it embodies a conscientious approach to financial stewardship, emphasizing transparency and integrity in transactions. His analysis encourages readers to appreciate the deliberate balance between convenience and responsibility embedded within financial instruments.

Building on Edward Philips’ thorough analysis, the crossed cheque emerges as a crucial instrument that combines practical security with ethical responsibility in financial transactions. Its defining feature-restricting payment to bank deposits-serves not only to prevent direct cash encashment and reduce fraud risks but also to enforce transparency through traceable banking channels. This mechanism effectively fortifies both the issuer’s and the recipient’s confidence in the transaction, transforming what might seem a simple payment tool into a symbol of mutual trust and accountability. Philips highlights how this traditional practice remains highly relevant, especially as financial systems evolve in response to new challenges. The crossed cheque thus exemplifies how established financial instruments can uphold integrity and conscientious stewardship amidst growing complexity, reminding us that thoughtful controls can coexist with convenience in responsible money management.

Building further on Edward Philips’ insightful analysis and the valuable perspectives shared, the crossed cheque indeed exemplifies how traditional financial tools can embody both security and ethical responsibility. By enforcing the requirement that funds be credited through banking channels rather than cashed directly, crossed cheques provide a vital layer of control that safeguards against fraud and enhances transaction traceability. This practice fosters a culture of accountability and trust between issuer and recipient, emphasizing that financial exchanges are not merely transactional but also relational and principled. In today’s digital age, where convenience often competes with caution, the crossed cheque reminds us that thoughtful mechanisms rooted in transparency and stewardship remain essential. It encourages a reflective approach to money management, blending procedural rigor with the timeless values of integrity and mutual assurance in financial dealings.

Adding to Edward Philips’ insightful exposition, the crossed cheque exemplifies how a seemingly simple financial tool can embody profound principles of security and ethical accountability. By mandating that payment be made strictly through bank deposit, this instrument not only safeguards the issuer’s funds but also fortifies the recipient’s confidence in the legitimacy of the transaction. The two parallel lines inscribed on the cheque symbolize more than a procedural requirement-they denote a commitment to transparency, traceability, and mutual trust. In an era where digital transactions dominate yet fraud risks persist, understanding the crossed cheque’s role highlights the enduring importance of cautious financial stewardship. Moreover, it invites a broader reflection on how traditional instruments adapt to uphold integrity amid evolving economic complexities, reminding us that responsibility and trust remain foundational pillars in all monetary exchanges.

Adding to the insightful reflections of Edward Philips and the previous commentators, the crossed cheque indeed illustrates a powerful intersection of tradition and prudence within financial operations. Beyond its procedural implications, the restriction to deposit-only channels fosters an environment where accountability is structurally embedded, thus reducing vulnerabilities to fraud and misappropriation. This deliberate act of crossing a cheque underscores a proactive approach to risk mitigation, emphasizing that secure financial exchanges stem not solely from technology but also from thoughtful design and intent. In a time when rapid digital payments often prioritize speed over scrutiny, the crossed cheque reminds us that safeguarding trust requires mindful measures that encourage transparency and mutual responsibility. Ultimately, mastering such nuanced payment instruments enriches our financial literacy and reinforces foundational values essential to maintaining integrity in monetary transactions.

Building on Edward Philips’ comprehensive exploration and the rich insights offered by previous commentators, the crossed cheque indeed stands as a timeless emblem of prudent financial governance. By mandating payment exclusively through bank deposits, it not only curtails the risk of theft and fraud but also enforces a transparent audit trail that bolsters trust for all parties involved. This dual parallel line transcends mere formality, serving as a powerful symbol of deliberate control and mutual accountability in an era increasingly dominated by digital transactions. The crossed cheque exemplifies how traditional instruments continue to evolve, balancing security with the convenience demanded by modern commerce. Ultimately, it reminds us that integrity and careful stewardship remain indispensable cornerstones of effective financial exchanges, reinforcing meaningful connections between issuers and recipients beyond the mere transfer of funds.